After a hailstorm blows through, you might look up at your roof and breathe a sigh of relief. From the ground, everything can look perfectly fine. But that's the tricky thing about hail—the real damage is often invisible to the untrained eye, quietly setting the stage for future leaks and a much shorter lifespan for your roof.

Getting a proper hail damage roof repair in Western Pennsylvania starts with knowing what you're actually looking for.

What Hail Really Does to Your Western Pennsylvania Roof

When a hailstorm hits Western PA, the damage to your roof is rarely obvious. It’s not like a tree branch has fallen and punched a hole through it. Instead, hail delivers a thousand tiny blows that add up, compromising your shingles in ways you won't notice until the first leak appears months later.

Asphalt shingles, which cover the vast majority of homes in our area, are especially vulnerable. A small piece of hail traveling at high speed can cause two main types of damage, and understanding them is key to protecting your home.

The Hidden Impact of Granule Loss

Take a close look at an asphalt shingle. It’s covered in a layer of tiny, sand-like granules. These aren't just for color—they're the shingle's first line of defense against the sun. They block the UV rays that bake the asphalt, causing it to become brittle and age prematurely.

Hail acts like a sandblaster, knocking these protective granules loose. The first sign you'll see is a collection of black granules in your gutters and at the bottom of your downspouts. This granule loss is a big deal because it exposes the raw asphalt to the sun, dramatically accelerating your roof's aging process and making it prone to cracking.

Understanding Shingle Bruising and Cracking

A much more serious problem is something we call shingle bruising. This is what happens when a hailstone hits hard enough to fracture the fiberglass matting inside the shingle. On the surface, it might only look like a dark, soft spot—a lot like a bruise on an apple. You can actually feel the indentation with your finger.

Expert Insight: Shingle bruising is the #1 thing homeowners and inexperienced inspectors miss. It’s not just a cosmetic scuff; it’s a structural failure. That soft spot is where the shingle has lost its integrity, making it unable to shed water effectively.

That "bruise" is a major weak point. Here in Western Pennsylvania, with our constant freeze-thaw cycles, a tiny fracture can quickly expand. Water gets in, freezes, widens the crack, and thaws, letting more water in the next time. Eventually, you have a full-blown crack, giving water a direct path to your roof deck, insulation, and eventually, your ceiling.

The weather patterns here don't help. Counties like Allegheny, Beaver, Butler, Washington, and Westmoreland are consistently hit with storms producing hail of at least ¾ inch in diameter. With storm season peaking from April through September, our roofs are under constant threat. Even if the damage isn't obvious right away, this kind of hidden wear and tear rapidly ages a roof, leading to leaks and mold if not caught early. You can explore more about how storm events impact homeowners in our region and learn about protecting yourself.

Why a Professional Inspection Is Essential

The true cost of hail damage isn’t fixing the immediate issue; it's the slow, cascading failure of your entire roofing system. A single storm can easily knock several years off a 30-year roof's life.

Think about it:

- Look for Clues: If you see dents in your gutters, air conditioner fins, or siding, it's almost certain your roof has taken a beating, too.

- Damage Gets Worse: A few missing granules might not seem like much, but after a few seasons of rain, snow, and ice, it can turn into a major leak.

- Insurance Has a Clock: Most homeowner's insurance policies have a strict time limit for filing a storm damage claim. If you wait too long to discover the damage, you could be on the hook for the entire repair cost.

This is why getting a professional roof inspection after a major hailstorm is so critical. An expert knows how to spot the subtle signs of bruising and granule loss that lead to big problems. They can provide the right documentation for a successful hail damage roof repair in Western Pennsylvania claim, turning a potential disaster into a manageable repair.

Your First Moves After a Hailstorm Hits

The storm passes, and that unnerving silence sets in after the racket of hail hammering your house. It’s natural to want to grab a ladder and see the damage up close, but please, don't. A roof slick with rain and ice is one of the most dangerous places you can be. Your safety comes first, always.

The good news is, you can learn a lot from a safe inspection right from the ground. A quick walk around your property can tell you just about everything you need to know to decide if it's time to call in a pro for hail damage roof repair in Western Pennsylvania.

Ground-Level Damage Assessment

Start by taking a slow walk around your home's perimeter. Often, the story of what happened on your roof is written all over the rest of your property.

Keep an eye out for these classic tell-tale signs:

- Dented Gutters and Downspouts: Your aluminum gutters, downspouts, and the fascia behind them are soft metal. If they have dents and dings, it's almost a guarantee your shingles took a beating, too.

- Damaged Siding and Window Screens: Look closely at your siding for any cracks or chips. Check your window screens for holes or tears. This tells you the hail was big enough and hit with enough force to cause real problems.

- Impact Marks on Decks or Patios: Painted or stained wood surfaces, like a deck, are great for spotting hail impacts. You’re looking for fresh, circular marks or little chips where the hailstone struck.

- Damaged Air Conditioner Fins: Those thin metal fins on your outdoor AC unit are incredibly fragile. If you see them flattened or smashed, that’s a very strong clue the hail was significant.

If you spot any of this collateral damage, it's a safe bet your roof is compromised. Now, it's time to see if any problems have made their way inside.

Checking for Interior Water Intrusion

Even a small leak might not show up as a puddle on your floor right away. The first signs are often much more subtle. Head upstairs and carefully check your ceilings and attic for any new evidence of moisture.

Homeowner Tip: Grab a good flashlight and head into your attic. Shine the light on the underside of the roof decking. What you're looking for are dark spots on the wood, damp-looking insulation, or, in the worst case, actual drips of water. These are major red flags that hail has punched through your roof's defenses.

If you do find an active leak, your immediate job is damage control. Place a bucket or a plastic bin directly underneath the drip. If it's coming down fast, a large trash can will do the trick. This simple action can be the difference between a small repair and having to replace entire sections of drywall and flooring.

The Power of Documentation

Before you touch anything—don't move debris, don't wipe up water—pull out your smartphone. Right now, your most important job is to document everything. This evidence is what will make or break your insurance claim.

- Take Photos: Get wide shots of each side of your house. Then, get up close and personal with the damage you found: the dented gutters, the cracked siding, that smashed AC unit.

- Record Videos: A slow walk-around video is perfect for showing the overall condition of your property. If you have a leak inside, get a video of the water dripping. It's powerful proof.

- Document Everything: Don’t forget to photograph any water stains on your ceilings or walls. Snap a picture of the buckets you've put out to catch the water, too.

This visual record creates an undeniable timeline and shows the immediate impact of the storm. Once you have this ammo in your back pocket, you’re ready to make two important calls: one to your insurance company, and one to a trusted local roofer.

Making the Call: Navigating Your Roof Damage Insurance Claim

With your emergency tarps in place and a camera roll full of evidence, it’s time to move on to the part that worries most homeowners: the insurance claim. I get it. The paperwork, the phone calls, the jargon—it can feel overwhelming. But approaching it with a solid game plan is the key to getting the money you’re owed for a complete and proper hail damage roof repair in Western Pennsylvania.

Your first move is straightforward. Call your insurance company or use their website/app to report the damage and get a claim started. Have your policy number handy. This is also when you’ll want to send over those initial photos and videos you took. They are your best opening argument.

The Adjuster's Visit: What to Really Expect

Once your claim is open, the insurance company will send out a claims adjuster. Their job is to inspect your property, verify the damage, and write up an estimate for the repairs. This inspection is a make-or-break moment for your claim.

Here’s the thing, though: insurance adjusters are only human. After a big hailstorm blows through our area, they are often swamped, running from house to house. A quick, 20-minute look-see from the ground might not catch the subtle but critical damage—like the widespread granule loss or the tiny, hard-to-spot bruises hail leaves on shingles. This is exactly where having an expert in your corner pays off.

A Pro Tip from the Field: Never, ever let an insurance adjuster inspect your roof alone. Have your trusted local roofing contractor meet them on-site. Your roofer is your advocate. They know precisely what to look for and can point out every single hail impact, ensuring nothing gets overlooked. This one step can be the difference between a denied claim and a fully funded roof replacement.

Having a roofer there ensures a level playing field. They speak the same technical language as the adjuster and can present the damage in a way that’s hard to dispute, preventing legitimate hail impacts from being brushed off as normal "wear and tear." Understanding how new technologies like automated claims processing can also help speed things up on the backend.

Understanding the Insurance Paperwork

After the adjuster’s visit, you’ll get a scope of work and a settlement offer. This document is often packed with confusing terms, but if you can get a handle on a few key concepts, you’ll be in a much stronger position.

The two numbers you absolutely need to understand are:

- Actual Cash Value (ACV): Think of this as the "used" value of your roof. It's what the roof was worth the moment before the storm hit, calculated by subtracting depreciation (for age and wear) from the full replacement cost. Your first check from the insurance company will almost always be for the ACV amount, minus your deductible.

- Replacement Cost Value (RCV): This is the big number—the total cost to replace your roof with brand-new materials of a similar kind and quality today. You won’t get this full amount upfront. You receive the rest of the money (the "depreciation") after the work is done and you send the final invoice to your insurer.

And of course, your deductible is the portion you pay out of pocket. This amount is subtracted from your total claim settlement.

For a deeper dive, especially for homeowners in Western Pennsylvania, you can explore our complete guide on the roof insurance claim process.

Your goal is simple: make sure the adjuster's final report includes everything needed to bring your roof back to its pre-storm condition. If their estimate seems low or they missed something, don't just accept it. A good roofer will help you challenge it by filing a supplement with more evidence, ensuring you have the funds for a quality hail damage roof repair in Western Pennsylvania.

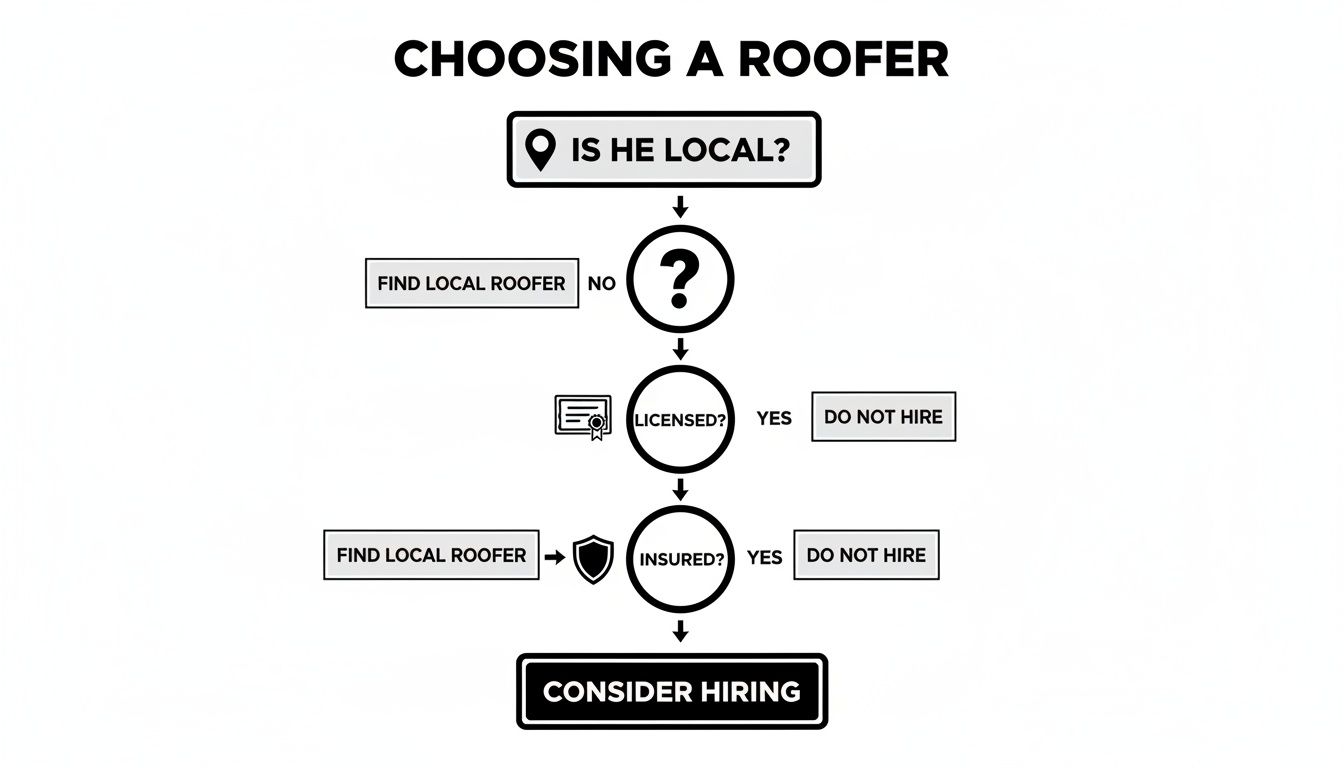

Finding a Trustworthy Local Roofing Contractor

After a hailstorm barrels through your Western Pennsylvania neighborhood, the sound of hail on the roof is quickly replaced by the sound of knocking on your door. Almost overnight, you'll be swamped with offers from "storm chasers"—out-of-town crews who follow bad weather, promising quick work and unbelievable prices.

Be careful. Hiring one of these transient outfits is one of the biggest gambles a homeowner can take. We’ve seen the aftermath far too many times: shoddy work, cheap materials, and a contractor who’s long gone by the time the first leak appears. A proper repair or replacement depends on finding a roofer who is part of our community and will stand behind their work for years, not just until the next storm hits another state.

The Good Guys vs. The Storm Chasers

Telling a reputable local pro from a fly-by-night storm chaser can be tough, especially when they’re all saying the same things. They’re masters of disguise, often using a local phone number and a slick sales pitch. But when you know what to look for, the warning signs become obvious.

Here's a quick checklist to help you separate a legitimate contractor from a potential scammer.

Reputable Local Roofer vs. Storm Chaser Checklist

| Attribute | Reputable Local Contractor | Storm Chaser Warning Signs |

|---|---|---|

| Physical Presence | Has a permanent, verifiable office or showroom in Western PA that you can visit. | Uses a P.O. Box, a hotel address, or has no local address at all. |

| Licensing | Is registered with the PA Attorney General (HIC #) and readily provides their number. | Avoids the topic, can't provide a valid HIC number, or claims it's "not needed." |

| Insurance | Carries full General Liability and Workers' Comp; provides certificates upon request. | Is vague about coverage, has out-of-state insurance, or pressures you to sign without verification. |

| Vehicles & Crew | Uses clearly marked company trucks and has an established local crew. | Shows up in unmarked personal vehicles or trucks with temporary magnetic signs. |

| Local Proof | Can give you addresses of recent projects completed in your town or county to see their work. | Offers a generic portfolio or references from people in another state. |

| Pressure & Payment | Provides a detailed estimate and allows you time to decide. Never asks for large upfront payments. | Demands an immediate decision, pressures you to sign a contract on the spot, or asks for a large cash deposit. |

A true professional will welcome your questions and have all this information ready. If a contractor gets defensive or gives you excuses, that’s your cue to thank them for their time and show them the door.

The Non-Negotiables: Insurance and Licensing

Let's focus on the absolute deal-breakers. Before you even think about signing a proposal, any roofer you speak with must prove they are licensed, bonded, and fully insured. This isn't just good practice—it's your primary protection as a homeowner.

- Pennsylvania HIC License: Any contractor doing more than $500 in home improvements must be registered with the Attorney General. This is the law, period.

- Full Insurance: This is the big one. They need General Liability to cover any damage to your property and Workers' Compensation to cover their crew. If a worker gets hurt on your roof and the contractor isn't insured, you could be held liable for their medical bills.

A roofer who hesitates to show you their insurance certificates is a roofer you don’t want on your property. There are no valid excuses. A professional will have this documentation on hand and be happy to provide it.

Some of the most thorough contractors now use modern tools like drone inspection services to get a safe, comprehensive look at every inch of your roof without anyone having to set foot on it. It’s a great sign of a professional who invests in accuracy and safety.

For a deeper dive into the vetting process, our full guide on how to choose a roofing contractor has even more tips.

Why Local Knowledge Matters

Finally, don’t discount the value of a roofer who truly gets our local weather. A contractor from a state with a milder climate simply won’t have the hands-on experience with Western PA’s brutal freeze-thaw cycles or the specific challenges posed by lake-effect snow.

A roofer based in Mercer, Beaver, or Lawrence County knows which materials and installation techniques actually last here. They’re also familiar with the specific building codes in each township, ensuring your project is done right and fully compliant. That kind of regional expertise is something an out-of-towner can't learn from a manual, and it's what makes a new roof a long-term, reliable investment.

Deciding Between Roof Repair and Full Replacement

So, a hailstorm just rolled through. Now you're facing the big question: can you get away with a simple patch job, or is it time for a whole new roof? This is where a lot of homeowners get stuck, but figuring out whether to repair or replace is crucial for protecting your investment and your home itself.

The right call really comes down to a few things: how old your roof is, how bad the hail damage actually is, and what kind of roofing material you have. If you have a fairly new roof with just a few dings here and there, a targeted repair is probably your best bet. But if you're looking at an older roof with widespread granule loss, a full replacement is often the only way to truly restore its protective barrier.

Assessing the Damage and Your Roof's Age

Let's start with your roof's age. Most architectural shingle roofs common here in Western PA are built to last somewhere between 20 to 30 years. If your roof is only five years old and has a couple of isolated impact marks, a professional roofer can typically swap out the damaged shingles and make it look like nothing ever happened.

It's a completely different story if your roof is pushing the 15-year mark or older. At that age, shingles are already more brittle. A hailstorm can be the final blow, causing extensive bruising and shedding the protective granules that shield your roof from the elements. Trying to patch a roof in this condition is like putting a bandage on a major wound—you'll just be chasing new leaks and problems every season.

A Pro's Rule of Thumb: If more than 25-30% of your roof's surface has been hit, a full replacement is almost always the smarter, more cost-effective choice in the long run. Patching widespread damage is a losing battle that often leaves your roof looking like a checkerboard.

This is also where finding the right contractor comes into play. You need an honest assessment from someone who knows what they're looking at.

As the chart shows, your first move should always be to confirm your roofer is local, properly licensed, and fully insured. Don't even look at a proposal until you've checked those boxes.

Realistic Costs for Repair vs. Replacement

Money is always part of the equation, and the cost for hail damage work in our area can swing pretty widely.

- Minor repairs, like replacing a handful of shingles or resealing a vent pipe, might cost anywhere from $500 to $2,500.

- Full replacement is a much bigger project, with costs running into the thousands. The final price tag depends on your home’s square footage, the complexity of your roofline, and the specific materials you choose.

For roofs in that 10-20 year old range, hail damage often tips the scales toward replacement. A series of small repairs can quickly add up and become more expensive than just starting fresh, especially with our harsh freeze-thaw cycles. If you're seeing more than just a few hail hits, it's worth learning about the other signs that indicate you need a new roof.

Understanding the Project Timeline

Whether you're looking at a small repair or a full-blown replacement, knowing the timeline helps manage the stress. A simple repair might be done in a few hours. A total roof replacement, on the other hand, is a more orchestrated process that usually takes a couple of days.

Here’s a look at what you can expect during a typical replacement:

Prep Work (Day 1, Morning): The crew shows up bright and early to get started. Their first job is protecting your property—they’ll cover landscaping, siding, and windows with tarps. A dumpster will also be placed in the driveway for the debris.

Tear-Off (Day 1, Morning/Afternoon): This is the noisiest part of the job. The crew will strip off all the old shingles and underlayment right down to the bare wood roof decking.

Decking Inspection (Day 1, Afternoon): Once the old roof is gone, the crew can get a clear look at the decking. They’ll inspect for any soft spots, water damage, or rot and replace any compromised wood before moving on.

Installation (Day 1-2): Now the new roof goes on. This includes a fresh layer of underlayment, critical ice and water shield in the valleys and eaves, and finally, the new shingles. A good crew works efficiently, and you’ll see the new roof take shape surprisingly fast.

Cleanup & Final Walkthrough (Final Day): The job isn't done until your yard is spotless. The crew will do a thorough cleanup, using magnetic rollers to snag any stray nails. Before they pack up, you’ll do a final walkthrough with the project manager to make sure everything looks perfect.

Your Top Questions About Hail Damage and Roof Repair Answered

When a hailstorm rips through Western Pennsylvania, the same worries pop up for homeowners across the region. Feeling lost in the aftermath is completely normal. Getting clear, honest answers is the best way to get back on solid ground, so let's tackle the most common questions we hear every day.

How Long Do I Really Have to File a Hail Damage Claim in PA?

This is a big one, and you need to get it right. Most homeowners insurance policies in Pennsylvania give you one year from the date of the storm to file a claim. But don't treat that as a guarantee—some policies have different timelines.

The best advice I can give you is to act now. Don't wait. The longer you put it off, the easier it is for an insurance company to argue that the damage came from a later storm or was caused by neglect. Your safest bet is to check your policy documents or call your agent to confirm your specific deadline, but get the ball rolling immediately.

Will Filing a Hail Claim Make My Insurance Rates Go Up?

It's the fear that stops too many homeowners from getting the repairs they're owed. The good news? In most situations, an insurer can't legally single you out for a rate hike just because you filed a claim for storm damage. It’s considered an "Act of God," and you're not at fault.

What's important to understand is the difference between an individual rate increase and a regional one. While your premium shouldn't jump from a single storm claim, rates for an entire area—like a zip code or county—can rise if that region sees a surge in claims from severe weather over time.

This is a huge reason why it’s so critical to work with honest, local roofers. Widespread fraud from out-of-town "storm chasers" can inflate claim costs for the whole community, which can eventually lead to higher rates for everyone in Western Pennsylvania.

What if My Insurer's Estimate is Lower Than My Contractor's?

First, don't panic. This happens all the time. An insurer's initial estimate is often just their opening offer. Adjusters are human; they can miss specific damage, miscalculate the amount of materials needed, or simply not be aware of local building codes that impact the cost.

This is where having a seasoned local roofer in your corner makes all the difference. When their estimate is higher, they will file a supplemental claim with your insurance company. Think of it as a formal, evidence-backed request for the additional funds needed to do the job right. This typically includes:

- Photos documenting the damage the adjuster missed.

- Line items for necessary materials that were left out (like specific types of flashing or ice and water shield).

- Citations of local building codes that require certain installation techniques or materials.

A roofer who truly specializes in hail damage roof repair in Western Pennsylvania lives and breathes this process. They will go to bat for you, handling the negotiations to make sure your claim covers the full cost of a proper, code-compliant repair.

Can I Just Keep the Insurance Money and Not Fix My Roof?

This might seem like a tempting way to pocket some extra cash, but it’s a bad idea with serious financial risks. It’s a move you’ll almost certainly come to regret.

For starters, your mortgage company gets a vote. If you have a mortgage, the lender is almost always named on the insurance check. They won’t release the full payment until you provide proof that the repairs have been completed. It's how they protect their investment in your home.

More importantly, you're taking on all future liability. If you skip the repairs and your roof starts leaking a year from now, your insurance company has every right to deny the new claim. Why? Because you failed to perform the original repairs they paid you for. You'd be setting yourself up for a much larger, entirely out-of-pocket expense down the line.

If you're dealing with hail damage and want an honest, professional opinion, put your trust in the local experts who have been serving this community for over 25 years. Contact Penn Ohio Roofing & Siding Group today for a free, no-obligation inspection and get the peace of mind you deserve. Visit us at https://pennohiorc.com to get started.