When a storm rolls through New Castle, the roof is usually the last thing you can really inspect and the first thing that can cost you. You step outside, see a few shingles in the yard, maybe find granules in the downspout, and suddenly you’re trying to make decisions that affect your home, your claim, and your premiums.

That’s where homeowners get into trouble. They either wait too long, file too fast, or trust a quick glance from the ground. An Insurance roof inspection New Castle PA isn’t just about spotting damage. It’s about proving what happened, when it happened, and whether your insurance carrier is likely to treat it as a covered loss instead of wear and tear.

In Lawrence County, local weather matters more than generic online advice lets on. Ice dams, Nor’easters, lake-effect weather, and spring hail don’t leave the same evidence. If the damage isn’t documented the right way, the claim can stall even when the roof clearly took a hit.

After the Storm Navigating Your First Steps

A lot of calls start the same way. A homeowner finds shingles near the driveway, notices a damp ceiling spot, or hears from a neighbor that hail came through harder than expected. The storm is over, but then the stress begins when you have to decide whether to call insurance, call a roofer, or do nothing and hope it’s minor.

That hesitation is understandable. Filing too early can create a headache if the damage doesn’t justify a claim. Waiting too long can make it harder to show that the damage came from one event.

Start with proof, not guesses

The first move is simple. Get a professional inspection before anyone starts talking about scope, payout, or replacement. Insurance carriers usually cover roof repairs or replacement when the damage comes from a covered peril such as hail, wind, fire, or falling objects, but they don’t cover ordinary aging. That distinction decides the claim.

A significant hail storm hit New Castle on April 14, 2024, causing widespread roof damage and a wave of insurance claims, which put a spotlight on how important timely professional assessments are in this area, according to local storm damage reporting for New Castle.

That event changed how many homeowners here think about inspections. It also changed how carriers look at documentation after major weather events.

What to do in the first day

Don’t climb the roof yourself. That creates a safety risk and usually doesn’t help your claim.

Use this first-day checklist instead:

- Walk the perimeter: Look for shingles, metal flashing pieces, gutter damage, and tree debris from the ground.

- Take ground-level photos: Capture every side of the house, detached garage, sheds, and any visible impact points.

- Check inside: Look in the attic and top-floor ceilings for fresh stains, damp insulation, or active drips.

- Pull your policy information: You’ll want the carrier name, policy number, and declaration page ready.

- Review visible warning signs: This guide to roof damage warning signs helps homeowners sort obvious storm evidence from older roof issues.

Practical rule: The goal on day one isn’t to diagnose the whole roof. It’s to preserve evidence and avoid mistakes.

The homeowner who does best in this process usually isn’t the one who reacts fastest. It’s the one who gets the roof inspected before making an insurance move they can’t take back.

Decoding Your Insurance Policy Before the Inspection

Most homeowners don’t read their policy until there’s a problem. That’s normal. But before the inspection results start coming in, you need to understand how your carrier looks at roof damage and what kind of payment structure you may be dealing with.

If you don’t know that, it’s easy to misunderstand a claim decision. Some people think they’re fully covered when they aren’t. Others assume a denial means the roof is fine. It doesn’t.

The terms that change your claim

Two policy terms matter right away.

Replacement Cost Value, often shortened to RCV, generally means the policy is designed around what it costs to repair or replace covered damage with comparable materials, subject to policy terms and your deductible.

Actual Cash Value, or ACV, usually means depreciation gets factored in. On an older roof, that can change the economics of the claim in a big way.

Then there’s your deductible. That’s the amount you’re responsible for before insurance pays the covered portion. If your storm damage doesn’t exceed that amount by much, filing may not make sense.

Why pre-claim inspection matters more now

Pennsylvania homeowners are dealing with a different insurance environment than they were a few years ago. By 2025, policy changes made preemptive roof inspections more important for maintaining coverage, and insurers increasingly used drone and satellite technology for remote assessments that flag older roofs for repair requirements, according to this overview of roofing insurance changes in 2025.

That same source also notes a practical point many homeowners learn too late. Filing a claim without first confirming that the damage is likely above your deductible can lead to an unnecessary claim record and possible premium issues.

Covered peril versus excluded condition

In many cases, confusion often begins.

A policy may cover:

- Hail impact

- Wind damage from severe storms

- Fire

- Falling objects such as tree limbs

A policy usually won’t cover:

- Age-related wear

- Long-term neglect

- Deterioration that happened gradually

- Old repairs failing from normal service life

That doesn’t mean an older roof can’t have a valid storm claim. It means the inspection has to separate recent storm-created damage from pre-existing condition.

A roof can be old and still have covered storm damage. Age alone isn’t the deciding factor. Documentation is.

Questions to answer before the inspection report lands

Before you talk payout, ask these:

Is the roof on an ACV or RCV basis?

This affects what kind of settlement you may receive if the claim is approved.What is the deductible?

You need this number in mind before deciding whether to file.Are there endorsements for wind or hail?

Some policies handle those losses differently than general dwelling coverage.Has the insurer already requested a renewal inspection?

If yes, the roof issue isn’t just about this storm. It may also affect continued coverage.Do I have prior repair records?

Those can help show responsible maintenance and separate old work from new damage.

If you want a practical walk-through of how policy terms, inspections, and claim filing connect, this overview of the roof insurance claim process is a useful reference.

What doesn’t work

Homeowners run into trouble when they assume the carrier will “figure it out.” The carrier will evaluate the loss, but they won’t build your file for you. They also won’t always explain why one line item was included and another was excluded in a way that makes trade-offs obvious.

Read the declarations page. Confirm the deductible. Understand whether you’re dealing with replacement cost or depreciated value. That groundwork makes the inspection far more useful because you’ll know what the findings mean financially.

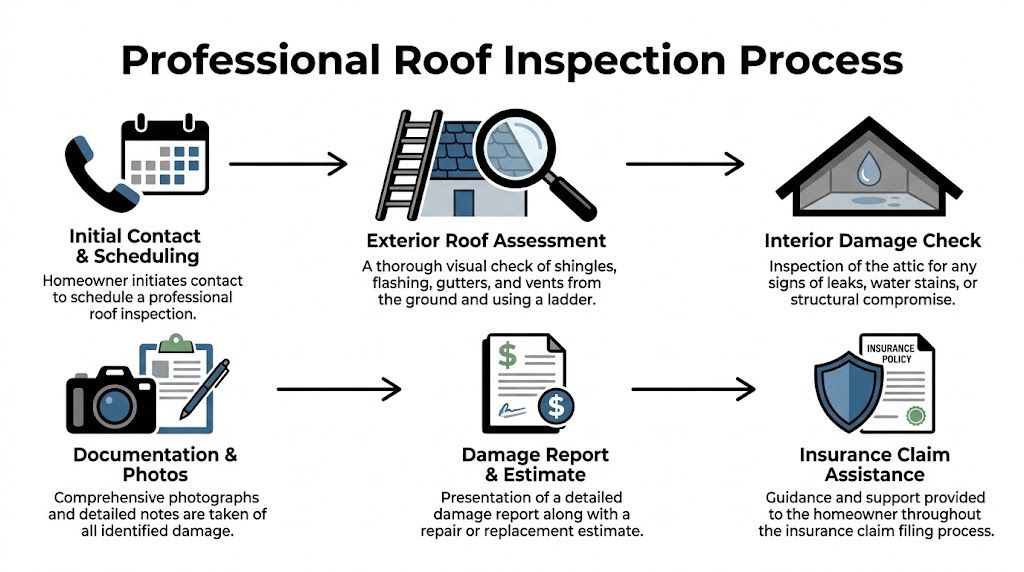

The Professional Inspection What to Expect Step by Step

A real insurance inspection isn’t a guy glancing at the roofline from your driveway. It’s a structured process. The point is to gather evidence in a format that an adjuster can use, challenge, or approve.

If the inspection is done right, it creates a paper trail. If it’s done poorly, you’re left with opinions.

Step one begins on the ground

The first thing we evaluate is safety and access. Wet slopes, high pitches, fragile decking, and storm debris all affect how the inspection gets done. Homeowners should never be the ones trying to “just take a look.”

From the ground, we’re already gathering clues. We look at missing tabs, bent gutters, downspout discharge, displaced flashing, fallen branches, soffit damage, and debris fields. Those details often tell the story of wind direction and impact severity before anyone gets near the main roof surface.

Exterior inspection means every component

Once access is safe, the inspection becomes systematic.

We check:

- Shingles: missing pieces, lifted edges, broken seals, creases, bruising, impact marks, exposed mat, and granule loss

- Flashing: step flashing, wall flashing, chimney flashing, valleys, and transitions where leaks commonly start

- Penetrations: pipe boots, vents, exhaust caps, skylights, and satellite mounts

- Drainage: gutters, downspouts, splash patterns, and overflow evidence

- Edges and ridges: starter strips, ridge caps, rake edges, and fastener exposure

Not every storm leaves obvious holes. In many New Castle claims, the question isn’t “is there damage?” It’s “can someone prove this pattern matches storm impact and not age?”

Interior evidence matters more than many people think

A roof claim isn’t only about what we see outside. Attic inspection and interior review can support or weaken the case.

We look for darkened decking, fresh staining, wet insulation, mold-like growth, daylight through penetrations, and ventilation imbalance. If a roof surface took damage weeks ago, the first visible symptom may appear inside long before a homeowner sees a missing shingle from the street.

Interior signs don’t automatically prove a covered event. They help connect roof failure to timing, location, and severity.

Why drones and thermal imaging changed the process

Modern inspections rely on better documentation than a phone camera and a clipboard. High-resolution photography matters because adjusters need location-specific evidence. Drone imaging matters because steep or complex roof lines hide a lot from ground view. Thermal tools matter because some storm damage doesn’t announce itself with a visible hole.

A professional roof inspection methodology uses high-resolution photos and drone-assisted thermal imaging to detect hidden problems such as heat loss or moisture, and that matters because those failures account for 70% to 90% of insured residential catastrophic losses, according to the inspection methodology summary citing IBHS data.

If you’re curious how aerial imaging fits into broader property assessment, this explanation of a Drone Inspection Service gives useful context on why roof professionals and insurers rely on it for hard-to-access surfaces.

The report is where claims are won or lost

Photos alone aren’t enough. The report has to organize the evidence in a way that ties cause, location, and urgency together.

A useful insurance report should include:

Date and property details

Exact address, storm date if known, roof type, slope notes, and building sections.Damage mapping

Which elevations or slopes show impact, wind lift, puncture, or water entry signs.Component notes

Specific findings on shingles, flashing, vents, gutters, ridge, valleys, and underlayment indicators.Supporting images

Wide shots for context and close-ups for proof.Repairability analysis

Whether localized repair is realistic or whether damage patterns point toward replacement.Insurance-ready language

Clear wording that distinguishes storm-created damage from age-related wear.

For homeowners who want to see what a properly structured file should look like, this guide to a roof inspection report for insurance lays out the standard.

What works and what doesn’t

What works is a repeatable process. Same checklist. Same photo standards. Same component review. Same reporting logic.

What doesn’t work is vague language such as “roof looks bad” or “probably hail.” Insurance carriers respond to documented conditions, not loose impressions. When the evidence is organized and the cause is explained clearly, the conversation with the adjuster changes immediately.

Your Essential Pre-Claim Documentation Checklist

The inspection report is only half the file. The other half comes from you. Homeowners who keep organized records usually have a smoother claim conversation because they can show what the roof looked like before, what maintenance was done, and what changed after the storm.

That matters even more on older homes. A roof that has a maintenance history looks different to an insurer than one with no paper trail at all.

Build a clean file before the claim gets noisy

Gather everything in one folder, digital or paper. Don’t scatter it across text threads, camera rolls, and kitchen counters.

Use this checklist as your working file.

| Document Type | Why It's Critical |

|---|---|

| Current insurance declaration page | Confirms carrier, policy information, and deductible reference point |

| Ground-level photos taken after the storm | Shows visible damage before cleanup or temporary repairs change the scene |

| Any safe pre-storm roof photos | Helps establish the roof’s prior condition |

| Attic or ceiling photos | Supports timing and location of water intrusion |

| Prior roof repair invoices | Shows the roof wasn’t ignored and helps distinguish older work from new storm damage |

| Full replacement paperwork if the roof was previously replaced | Helps establish age, materials, and installation history |

| Maintenance records | Supports a pattern of responsible ownership |

| Gutter cleaning or seal-check receipts | Useful because routine upkeep can support insurability arguments |

| Emergency mitigation receipts | Temporary tarping or leak control costs may matter in the claim file |

| Notes with storm date and observations | Creates a clear timeline while details are still fresh |

| Contractor inspection report | Gives the carrier a professional basis for evaluating the loss |

| Communication log with insurer | Tracks who said what and when |

Maintenance records carry more weight than people expect

In claim disputes, homeowners often focus only on the storm event. Carriers also look at whether the roof was maintained. A documented history of bi-annual maintenance, including routine work like clearing drains and checking seals, gives them an advantage during claim negotiations and strengthens insurability, especially on roofs over 15 years old, according to this commercial roofing inspection and maintenance overview.

That doesn’t mean you need a perfect binder full of records. It means every receipt, inspection note, and dated photo helps.

Keep your evidence simple and chronological

Don’t overcomplicate the file. Organize it in time order:

- Before the storm: prior photos, old invoices, maintenance notes

- Immediately after the storm: yard debris photos, gutter findings, interior leak signs

- Inspection stage: contractor report, annotated photos, recommendations

- Claim stage: call log, adjuster appointment notes, emails, estimate documents

The strongest file is usually the easiest one to follow. Clear dates beat long explanations.

A lot of claims slow down because the homeowner has the right information but can’t present it cleanly. If your roof took a legitimate hit, your documentation should make that obvious without forcing the adjuster to hunt for the story.

Navigating Local Challenges New Castle Weather and Your Roof

Insurance companies use broad standards. New Castle roofs fail in local ways. That gap causes problems.

A roof in Lawrence County takes a different beating than a roof in a mild climate. Snow load patterns, freeze-thaw cycles, wind-driven rain, and hail can leave damage that doesn’t look dramatic from the curb. If the person reviewing the claim doesn’t understand how western Pennsylvania weather affects roofing systems, storm damage can get labeled as age or neglect.

Why local weather changes the evidence

New Castle sits in a zone where Nor’easters and lake-effect weather can create repeated stress on shingles, flashing, eaves, and ventilation points. In 2025, NOAA recorded 15 severe thunderstorm warnings in Mercer and Lawrence Counties, and reporting tied that weather pattern to higher roof claim denials in western Pennsylvania because adjusters often misattributed damage to wear, according to this analysis of the insurance inspection process in the region.

That same source noted that ice dam formations caused a 35% spike in underwriting inspection failures in 2025. That matters because ice dam damage is one of the easiest local issues to misunderstand.

Ice dams don’t leave generic damage

Ice dams usually start at the eaves when melting snow refreezes and traps water uphill. That backed-up water can work under shingles and show up as stained decking, damp insulation, peeling paint, or interior ceiling marks.

The trouble is that an adjuster may see the leak and think “old roof” if the file doesn’t explain the weather mechanism. A local inspection needs to show the eave condition, ventilation pattern, insulation clues, and water path. Without that context, the evidence looks incomplete.

Wind damage here often looks subtle

In New Castle, strong wind doesn’t always tear half the roof off. More often, it breaks adhesive seals, lifts shingle edges, creases tabs, and loosens ridge material. From the ground, the roof can look mostly intact.

That’s where claims get tricky. A non-local reviewer may call it thermal aging or normal brittleness. A local contractor who knows how Nor’easter-driven gusts affect older laminated shingles will document the pattern differently.

Damage patterns that get misread

- Lifted shingle tabs can be mistaken for ordinary aging when the seal strip failure is storm-related.

- Granule loss near impact points can be dismissed as age if no one documents collateral signs on soft metals and accessories.

- Interior moisture near eaves can get treated as maintenance failure instead of ice dam backup.

- Flashing separation around penetrations may be written off as old caulk failure without noting wind-driven movement.

Local weather doesn’t excuse poor maintenance. It does change how real storm damage presents, and that has to be documented correctly.

The local context your claim needs

A proper Insurance roof inspection New Castle PA should do more than list damaged components. It should explain why those components failed in this climate.

That includes:

- Storm timing: matching observed damage to a known local weather event when possible

- Slope orientation: some roof faces take the brunt of prevailing storm conditions

- Eave behavior: critical for ice dam cases

- Ventilation and attic clues: useful when leak paths don’t match obvious exterior openings

- Material condition versus storm effect: showing the difference between an aged roof and a roof that suffered a covered event

Generic claim handling tends to flatten all storm damage into one category. In Lawrence County, that approach misses too much. Local weather leaves a local signature, and your inspection has to capture it if you want the claim reviewed fairly.

Working with Your Adjuster and Penn Ohio Roofing

Once the claim is filed, the adjuster becomes the gatekeeper. Their job is to evaluate the loss under the policy. Your job is to make sure the roof is evaluated completely, not casually.

Those aren’t always the same thing. Adjusters work under time pressure. They may inspect several properties in a day, especially after a major storm. That doesn’t make them the enemy, but it does mean homeowners shouldn’t walk into the meeting unprepared.

Why contractor presence matters

If you meet the adjuster alone, you’re relying on your own memory and their interpretation. If a roofing professional is present, questions get answered in real time. Damage areas can be pointed out on the spot. Missing line items can be raised before the first estimate hardens into the working scope.

That matters even more on aging roofs. For homes with roofs 15 years or older, insurers are increasingly requiring inspections for renewal, and if the initial adjuster report is incomplete, a GAF-certified professional can provide a supplemental report that may improve approval outcomes by as much as 30%, according to this roof assurance guide discussing aging-home inspections and supplemental reporting.

Penn Ohio Roofing & Siding Group can provide that kind of insurance-focused inspection documentation, including roof condition reporting and claim support based on certified findings.

What the adjuster often sees first

Adjusters usually focus on visible damage, repairability, and whether the observed condition fits the policy language. That means they may not initially include every accessory, flashing transition, or code-related need if it wasn’t obvious during the first visit.

That’s why the first estimate isn’t always the final word.

Items that often need a second look

Flashing and accessory replacement

The field shingles get attention. The surrounding system details sometimes don’t.Multiple test areas

One slope may show obvious damage while another has subtler but related failure.Interior consequences

Water staining, insulation issues, and deck moisture can lag behind exterior damage.Repair versus replacement logic

A roof might be technically patchable on paper and practically unserviceable in the field.

Supplemental claims are normal

A supplement isn’t a fight for the sake of fighting. It’s the process of submitting additional evidence when the approved scope doesn’t fully cover what the roof needs.

A good supplement package usually includes updated photos, precise line-item explanation, and a clear statement of why the initial scope is incomplete. The more organized that package is, the easier it is for the carrier to review.

A supplement should answer one question clearly. What was missed, and what evidence supports adding it?

Keep the adjuster meeting professional

The strongest approach is calm and specific.

Use these rules:

- Be factual: Stick to dates, observations, and documented findings.

- Take notes: Write down what the adjuster inspected and any concerns they raised.

- Ask for the scope in writing: You need the actual estimate, not a verbal summary.

- Avoid diagnosis from memory: Let the documented inspection lead.

- Follow up promptly: Delays create confusion and stall supplements.

There’s a practical reason good roofing teams stay organized after storms. Efficient scheduling affects everything from emergency tarping to adjuster attendance. If you want a clear explanation of how service teams reduce wasted trips and tighten response windows, this article on route optimization gives a useful operations view.

The main point is simple. When the adjuster visit is handled well, the claim becomes a documented review instead of a guessing contest.

Your Path to a Restored and Secure Roof

Most roof claims don’t go sideways because the damage wasn’t real. They go sideways because the evidence was thin, the timing was off, or the local weather story never got translated into a form the carrier could evaluate properly.

That’s why preparation matters. A good Insurance roof inspection New Castle PA combines policy awareness, careful documentation, local storm knowledge, and a disciplined inspection process. When those pieces are in place, homeowners make better decisions about whether to file, how to present the loss, and when to push for a supplement.

If your roof was hit by hail, wind, or winter weather in New Castle or the surrounding area, don’t guess from the yard and don’t rush into a claim blind. Start with a professional inspection, build a clean file, and make the carrier respond to documented facts.

If you need clarity on storm damage, policy renewal concerns, or an insurance-ready roof report, contact Penn Ohio Roofing & Siding Group for a free, no-obligation inspection. We serve homeowners and property owners across the New Castle area and can help you understand what the roof is telling you before you make the next insurance decision.