You walk out after winter, look up at the side of the house, and notice what wasn’t there last fall. A panel has lifted near the corner. Paint is peeling around older trim. You rub the wall and get a chalky residue on your hand. That’s usually the moment Mercer homeowners start searching for a siding contractor Mercer PA and realize how hard it is to separate a solid installer from a fast talker.

In this part of Pennsylvania, siding isn’t cosmetic. It’s the shell that stands between your sheathing and months of wet weather, snow load, wind, and repeated freeze-thaw movement. A bad install can look acceptable on day one and still fail years too early.

The good news is that most siding problems follow patterns. If you know what to look for, what materials hold up here, how estimates are built, and how storm claims should be documented, you can make a much better decision before signing anything.

Your Guide to Choosing a Siding Contractor in Mercer PA

A lot of siding projects start with a small symptom that homeowners try to ignore. One loose course near a gable. A soft spot under a window. A strip that rattles when the wind hits the west side of the house. Then spring rain shows up, and what looked minor starts feeling urgent.

Mercer County gives exteriors a rough workload. Pennsylvania sees an average of 45 to 50 inches of annual precipitation and regular freeze-thaw cycles that wear down home exteriors, which is one reason local demand for siding work stays high according to BuildZoom’s Mercer contractor data.

What a good contractor should actually do

A good siding contractor doesn’t just sell a color and hand over a quote. They inspect trim transitions, window and door penetrations, starter strips, housewrap condition, flashing details, and the areas where water usually sneaks in first. They should also explain whether your house needs a repair, a partial replacement, or a full tear-off.

That matters because the cheapest number on paper often skips the expensive parts you can’t see. Old moisture damage, uneven walls, rotted corners, and sloppy flashing don’t disappear because an estimate left them out.

Practical rule: If a contractor spends more time discussing color samples than wall prep, fastening, and water management, keep looking.

Why local judgment matters

Mercer homes vary a lot. Farmhouses, ranches, split-levels, and newer suburban builds all move differently and weather differently. A siding contractor Mercer PA homeowners can trust needs to account for exposure, shade, roof runoff, and the condition of the existing wall assembly.

That’s also where experience helps. Penn Ohio Roofing & Siding Group brings a family-run perspective from years of working on homes in this region, which matters when you’re dealing with storm wear, replacement planning, and the kind of practical trade-offs homeowners face.

Assessing Your Home's Siding Needs

A common Mercer call goes like this: wind-driven rain gets behind one loose section, the homeowner spots a stain days later, and then a second problem shows up when the insurance adjuster asks for photos from before the temporary repair. That is why the first step is not picking a product. It is figuring out what failed, how far it spread, and whether the damage looks like age, installation error, or a storm event.

Start from the ground and read the walls in order. Long, open runs usually show movement first. Corners, window heads, door trim, and lower courses near grade often show water entry first. If a hailstorm or wind event recently hit Mercer County, document what you see before anything gets disturbed. Clear photos of cracked panels, lifted laps, damaged fascia, dented gutters, and broken trim can make a real difference later if you need to handle a siding claim.

Start with a ground-level inspection

Walk the full perimeter slowly and look for patterns, not just isolated blemishes.

Use this checklist:

- Cracks or splits: Often tied to impact, cold-weather brittleness, or older siding that has lost flexibility.

- Warping or bowing: Usually points to bad fastening, heat distortion, or moisture trapped behind the panel.

- Loose sections: Wind may have broken the lock, pulled fasteners, or exposed an installation problem that was already there.

- Bubbling paint or swollen trim: Water is often getting in around windows, doors, roof lines, or utility penetrations.

- Rot at lower walls: Splashback near porches, decks, mulch beds, and foundations causes a lot of hidden deterioration in this area.

- Chalking or heavy fading: Age alone does not mean failure, but it does affect repair matching and can push a claim toward a disputed partial replacement.

- Interior clues: Drafts, damp smells, peeling paint, or staining on inside walls often trace back to an exterior leak path.

Take wider photos first, then close-ups. I also tell homeowners to note the date of the storm, the direction of the worst exposure, and whether gutters, downspouts, soffit, or roofing were hit too. Insurance carriers look for a cause. Good documentation helps separate sudden storm damage from long-term wear.

Repair or replace

A simple way to decide is to determine whether the problem is isolated or systemic.

Repair usually makes sense when damage is limited to one elevation, one corner, or one area around an opening, and the surrounding siding is still solid and available for a decent color match. Replacement becomes the better call when panels are brittle, multiple walls have failed, moisture has reached the sheathing, or previous patch jobs have created a pieced-together exterior that will keep costing money.

If the wall behind the siding is wet, soft, or moldy, surface repairs will not fix the actual problem.

This is also the stage where claim strategy matters. Insurance may pay for storm-related damage, but not for old housewrap, rotten sheathing from a long-term leak, or siding that was nearing the end of its service life before the storm. Homeowners get into trouble when they assume every visible defect belongs in the claim file. The stronger approach is to separate storm damage from deferred maintenance and have the contractor document both clearly.

Pay attention to where the failure is happening

Location often tells you more than appearance.

South and west walls usually take the hardest weathering from sun and repeated exposure. Lower courses absorb splashback and snowmelt. Walls below short overhangs or beside roof runoff points stay at higher risk because water reaches them more often and dries out more slowly. On older homes, I pay close attention to any area where siding dies into masonry, porch roofs, or additions built in a different era.

A contractor should inspect these transitions closely:

- Around windows and doors

- Where siding meets roofing

- At deck ledgers and porch roofs

- At inside corners and utility penetrations

Those spots turn a small leak into sheathing and framing repair.

Material style also affects what to inspect. Homes with textured profiles, vertical panels, or shake accents can hide damage differently than standard horizontal vinyl. If your house uses decorative accents, this guide to cedar shake siding installation details gives a good sense of the joints and edge conditions that deserve extra attention during an inspection.

One last practical point. If a storm is involved, do not let anyone rush straight to replacement numbers without first identifying the full scope of damage and preserving photo evidence. A careful inspection protects your budget whether you pay out of pocket or end up filing a claim.

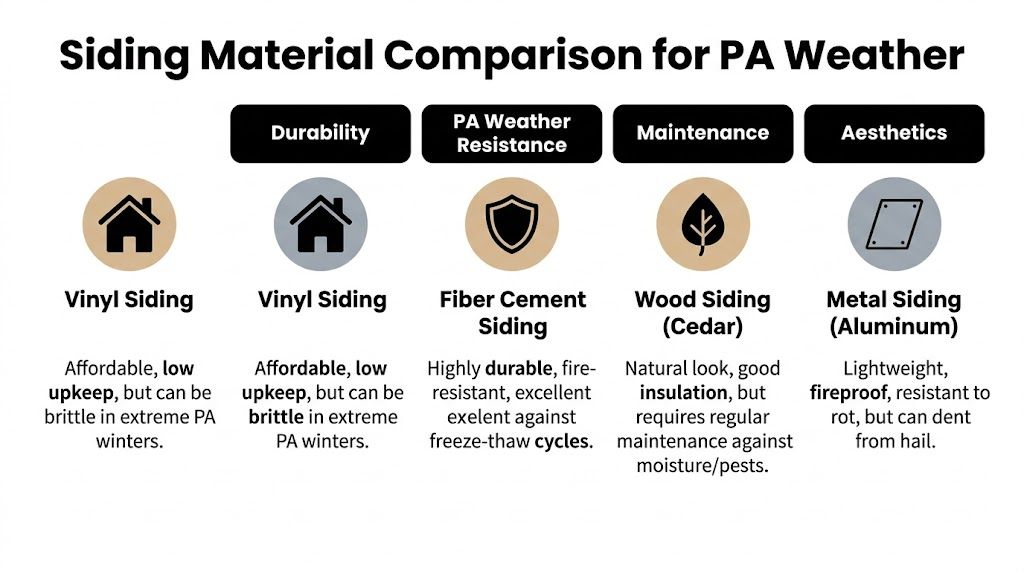

Comparing Siding Materials for Pennsylvania Weather

Material choice should fit the house, the budget, and the amount of maintenance you’re willing to live with. In Mercer County, the wrong choice usually doesn’t fail because the brochure was wrong. It fails because the product wasn’t matched to the climate, the wall condition, or the homeowner’s expectations.

Vinyl siding

Vinyl remains popular for a reason. It’s widely available, relatively low maintenance, and works well when it’s installed with room to move. That last part matters a lot here. For vinyl to perform in Mercer’s climate, installers should use a minimum 1-inch overlap and fasten with corrosion-resistant nails at 12 to 16 inch intervals so the siding can resist wind uplift exceeding 110 mph, as outlined in this vinyl siding installation guidance.

What works:

- Lower upfront cost

- Easier color and profile selection

- Little routine upkeep beyond cleaning

What doesn’t:

- Poor fastening leads to buckling and noise

- Cheap panels can look wavy on uneven walls

- Repairs can be obvious if color fade has set in

Insulated vinyl siding

Insulated vinyl takes the same basic idea and adds rigidity. On older homes with minor wall irregularities, that can improve the finished look. It can also help with comfort when the wall assembly is drafty.

The trade-off is price. You’re paying more than standard vinyl, and the result still depends on proper prep, trim work, and moisture management behind it. If the underlying sheathing is compromised, insulated siding won’t fix that.

Fiber cement siding

Fiber cement is a strong option for Pennsylvania weather. It has a Class A fire rating and dimensional stability that helps it resist cracking through the 50+ freeze-thaw cycles common in Mercer County annually, based on Mercer County fiber cement guidance.

What works:

- Better rigidity and impact resistance

- Strong performance in freeze-thaw conditions

- Crisp lines and a more substantial appearance

What doesn’t:

- Heavier material and more labor-intensive installation

- More demanding cut, flashing, and fastening details

- Higher project cost

Cedar and other specialty looks

Some homeowners want texture and a more traditional look, especially on dormers, gables, and accent walls. In those cases, cedar shake siding ideas and applications can make sense visually, but wood-based exteriors require a stronger maintenance commitment in a wet Pennsylvania climate. They can look excellent. They just aren’t hands-off.

Side-by-side comparison

| Material | Average Cost (per sq. ft.) | Lifespan | Pros for PA Climate | Cons for PA Climate |

|---|---|---|---|---|

| Vinyl | $5 to $10 | Often backed by long manufacturer warranties when properly installed | Affordable, low upkeep, flexible design options | Can buckle or separate if fastened incorrectly |

| Fiber cement | $12 to $18 | 30 to 50 years per manufacturer benchmarks in the verified data | Handles freeze-thaw conditions well, strong fire performance, more rigid finish | Higher install cost, heavier product, more complex detailing |

| Insulated vinyl | Qualitatively higher than standard vinyl | Varies by product and install quality | Improved rigidity and cleaner appearance on some walls | Still depends heavily on proper prep and moisture control |

| Cedar or wood siding | Qualitatively varies by grade and finish | Varies with maintenance | Natural appearance, useful for accents | More maintenance in wet conditions, more vulnerable to moisture issues |

| Aluminum or metal siding | Qualitatively varies | Varies by product and exposure | Won’t rot and can suit some home styles | Can dent from hail and may show impact damage |

Choose the material for the wall assembly you actually have, not the one that looks easiest in a sample book.

Budgeting Your Mercer PA Siding Project

A siding budget in Mercer often changes after the first hard rain or the first piece of old siding comes off. Homeowners expect to compare color and price. The actual budget usually turns on what is hiding underneath, how much detail work the house has, and whether storm damage may qualify for an insurance claim.

Most estimates break into four cost groups. Materials, labor, tear-off and disposal, and trim or accessory work. The spread between bids usually shows up in the last three.

For an average Mercer-area home, vinyl replacement often falls somewhere in the low five figures, while fiber cement comes in higher because the material is heavier and the install is slower. Exact numbers vary with house size, wall height, trim package, and how much repair work shows up during tear-off. If the house has hail strikes, wind damage, or brittle older panels, I tell homeowners to pause before approving work out of pocket. A documented storm claim can change the budget more than shaving a little off the contract price.

Where budgets go off track

Simple walls cost less. Cut-up houses cost more.

A ranch with long, open wall runs is faster to side than a two-story home with dormers, bump-outs, layered trim, porch tie-ins, and steep grade changes. Crews spend more time setting up, cutting around details, and finishing transitions cleanly.

The other common cost drivers are less visible at first:

- Sheathing repairs: Old leaks, swollen OSB, and soft spots only show once the siding is off.

- Flashing and water-management corrections: Missing kickout flashing, bad window tape details, and failed housewrap seams should be fixed before new siding goes on.

- Trim scope: Corners, frieze boards, window wraps, soffit transitions, and light block details add labor fast.

- Disposal costs: Heavy tear-offs, mixed materials, and long dump runs raise hauling charges.

- Storm-related documentation: If damage may involve insurance, photos, test squares, and matching paperwork add time up front but can protect you from paying for covered loss yourself.

Why one quote is thousands apart from another

The cheapest number is often the shortest scope.

One proposal may include full tear-off, wall inspection, damaged substrate replacement allowances, new weather barrier, proper flashing, and trim replacement. Another may cover basic siding installation with very little prep. On paper, both are siding quotes. In practice, they are different jobs with different risk.

Get clear line items. Ask what happens if the crew finds rotten sheathing. Ask whether soffit and fascia are included or priced separately. Ask who handles insurer documentation if the damage came after a wind or hail event. A contractor that works with adjusters regularly can save a homeowner from missing claim details that should have been documented on day one. If you want a rough starting point before appointments, this guide on how to measure vinyl siding helps you estimate wall area and understand how contractors build a number.

Budget for the claim process too

Storm damage budgeting is not just about the install price. It is also about timing, paperwork, and whether the siding can be matched.

If one elevation is damaged and the existing product is discontinued or badly faded, partial replacement can create a patchwork result. That is where contractor photos, manufacturer availability checks, and a clear scope matter. Homeowners looking at review history for companies that handle exterior claims can compare documentation habits and customer experience through sources such as A1 Roofing Kangaroof.

Good siding work costs money. Paying once for correct prep, moisture control, and claim documentation usually costs less than paying for avoidable repairs or an underpaid storm loss later.

How to Vet and Hire Your Siding Contractor

Hiring well is less about finding the smoothest salesperson and more about finding the contractor who documents everything, answers plainly, and doesn’t dodge detail work. A siding contract should read like a work plan, not a placeholder.

Ten questions worth asking

Ask these before you compare final numbers:

- Are you licensed, bonded, and insured in Pennsylvania? Ask for proof, not a verbal yes.

- Who is supervising the job daily? The estimator and the site lead are not always the same person.

- What prep work is included? Old siding removal, wall inspection, housewrap, flashing, and trim details should be spelled out.

- How do you handle damaged sheathing if you find it?

- What exact siding product and profile are you quoting? Brand, line, color, and accessory package matter.

- How will you fasten and flash this system? A real installer should answer comfortably.

- What warranties apply to labor and materials?

- Can you provide recent local references?

- What is the payment schedule? It should be tied to clear milestones.

- What is excluded from this proposal? This question reveals a lot.

For homeowners comparing reputations, third-party review collections can help as a secondary check. A page like A1 Roofing Kangaroof customer testimonials shows the kind of detail worth looking for in any contractor feedback, such as communication, cleanup, scheduling, and issue resolution. Reviews should support your decision, not replace proper vetting.

Red flags that deserve a hard no

- Large cash demand upfront

- Vague one-page contracts

- No product names listed

- Pressure to sign “today only”

- No explanation of flashing, trim, or wall prep

- No local references

- No written process for change orders

A cheap contract with missing scope often turns into an expensive project.

What a solid contract includes

A good agreement should identify the exact products, estimated timeline, payment schedule, cleanup expectations, warranty terms, and how hidden damage will be documented. It should also state who handles permits if they’re needed.

If you’re comparing companies that work on broader exterior systems, reviewing examples from a Mercer County home exterior contractor resource can help you see how siding intersects with trim, gutters, soffit, and roof edges. That overlap matters because wall protection is never just one component.

Navigating Siding Insurance Claims After a Storm

Storm-damaged siding is where many homeowners get frustrated. They know the wall doesn’t look right, but they aren’t sure what to photograph, when to call insurance, or how to respond if the first scope misses damage. That confusion is common. 68% of homeowners report dissatisfaction with how contractors handle insurance claims, and 2025 to 2026 windstorm trends increased claims by 22%, according to this insurance-claims discussion for siding damage.

What to do first

Start with safety. Don’t pull loose sections off the wall unless they’re creating an immediate hazard. Don’t climb onto wet roofs or ladders in unstable conditions.

Then document everything:

- Take wide photos first: Capture each elevation so the adjuster sees the full context.

- Add close-ups next: Cracks, punctures, lifted panels, broken corners, and detached pieces.

- Photograph collateral damage: Gutters, fascia, window wraps, shutters, and screens.

- Write a short timeline: Date of storm, what you observed, and whether water entered the home.

Why the contractor inspection should come early

A contractor inspection before or near the claim filing helps identify damage that homeowners often miss, especially at corners, lock seams, and transitions. This isn’t about inflating a claim. It’s about making sure the scope reflects what’s damaged.

Penn Ohio Roofing & Siding Group is one local option homeowners may call for an inspection and documentation review when siding damage appears after a storm. In practice, that kind of visit is most useful when the contractor can map damage by elevation and explain which components are related.

Understand the terms before you sign anything

Two claim terms matter a lot:

- Depreciation: This is the value the carrier may hold back based on age or condition, depending on your policy.

- Supplement: This is a request for added payment when hidden or newly documented damage appears after the original scope.

A lot of claim disputes come from homeowners approving work before the scope is complete. Read your policy language first. If you want a plain-language refresher on coverage basics, this guide on understanding your home insurance policy is a useful starting point for the terms most owners struggle with.

Meet the adjuster with your contractor if possible. It reduces missed items and cuts down on back-and-forth later.

Keep the paper trail clean

Save every estimate, claim email, adjuster summary, photo set, and change order. If replacement siding won’t match the undamaged walls, that should be documented early. Claims move more smoothly when the file tells a clear story from first inspection to final scope.

Why Mercer Homeowners Choose Penn Ohio Roofing & Siding

For a siding project in Mercer County, the standard is straightforward. Homeowners need clear communication, documented prep work, and experience with the freeze-thaw cycles, wind, and storm damage common in western Pennsylvania.

Penn Ohio Roofing & Siding Group gives homeowners a way to verify those basics. The company has more than 25 years of family-owned exterior experience in Mercer, Beaver, and Lawrence counties, and its background notes GAF Triple Excellence recognition. They are also described as licensed, bonded, and insured, which should be confirmed before any contract is signed.

That track record matters in the parts of a project that owners often do not see at first glance. Material matching, wall prep, trim details, disposal, and change-order handling are usually where jobs stay on track or start slipping. The same goes for storm work. If siding damage may involve an insurance claim, a contractor needs to document conditions clearly, explain what belongs in the scope, and keep the file organized enough that the owner is not sorting it out alone later.

That is the practical reason some Mercer homeowners call Penn Ohio.

If your siding is loose, weather-worn, or storm-damaged, contact Penn Ohio Roofing & Siding Group for a free, no-obligation estimate and ask direct questions about repair versus replacement, scope details, and whether the damage should be documented for an insurance review.