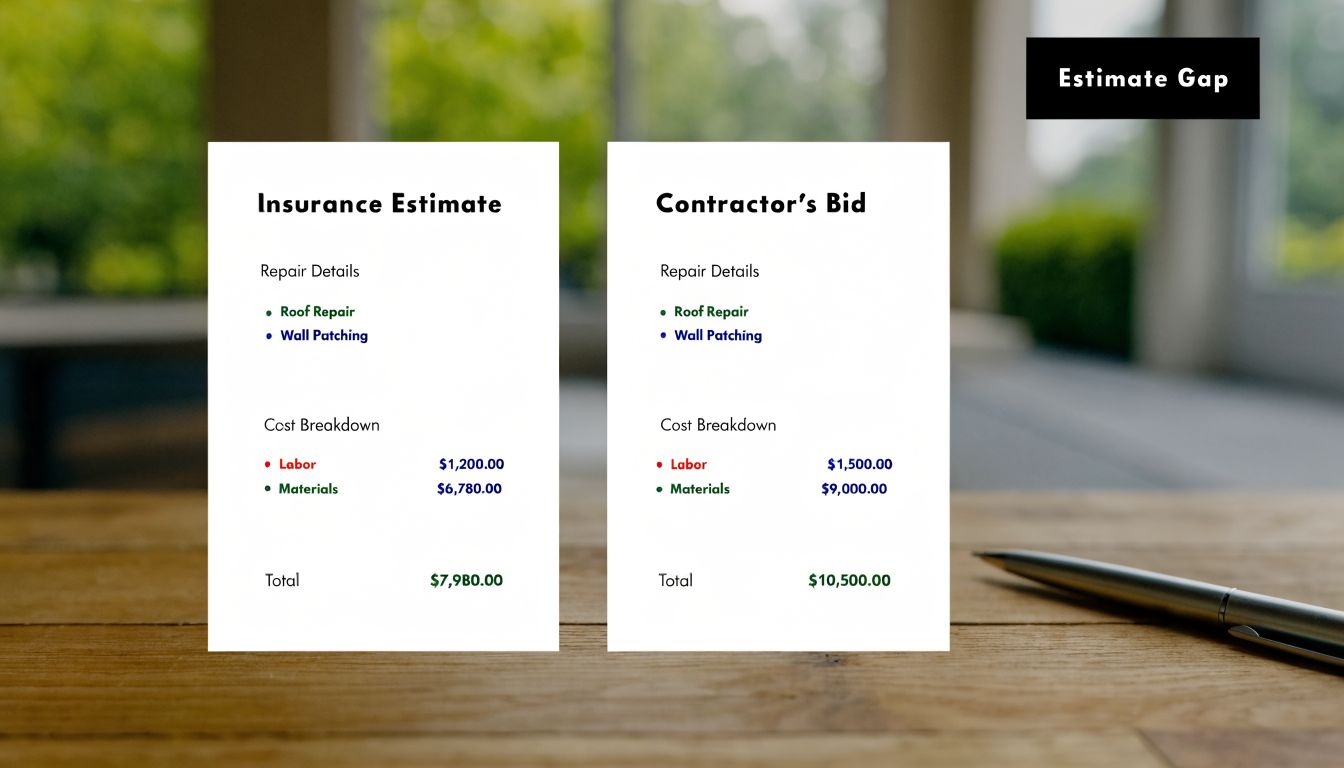

You open the insurance paperwork, compare it to the roofing bid, and the numbers don't line up. That's one of the most common claim questions homeowners ask after storm damage. It also creates immediate uncertainty. Did the adjuster overestimate? Did the roofer miss something? Are you allowed to keep the difference?

In many cases, a roof repair cost less than insurance estimate isn't a problem at all. It's a normal result of how carriers calculate claims versus how contractors price real work in local markets. The key is knowing whether the lower bid reflects efficiency and smart scope management, or whether it leaves out items that matter to your roof's long-term performance.

Table of Contents

- Why Your Roofer's Bid and Insurance Estimate Don't Match

- Your Action Plan When the Repair Cost is Lower

- Handling Insurance Checks, Deductibles, and Depreciation

- How to File a Supplement for a More Accurate Estimate

- Partnering with Penn Ohio Roofing for a Successful Repair

- Frequently Asked Questions About Insurance Surpluses

Why Your Roofer's Bid and Insurance Estimate Don't Match

The first thing to know is this. Different numbers on an insurance estimate and a contractor bid usually mean the two parties are pricing the job from different starting points.

Three reasons the numbers differ

The biggest reason is ACV versus RCV. Insurance companies often apply depreciation based on roof age. A common example is a roof with a $20,000 replacement cost that's 15 years old. Under an Actual Cash Value claim, the payout might be around $5,000 after depreciation, while a Replacement Cost Value policy could cover the full $20,000 for the same roof, as explained in SageSure's breakdown of ACV and roof replacement cost.

The second reason is pricing method. Adjusters often build estimates using standardized software and preset line items. A contractor prices the actual roof in front of them. That includes steepness, access, waste factor, flashing details, ventilation setup, and whether the repair can be done cleanly without opening up more sections than necessary.

The third reason is scope. Insurance paperwork may include items that won't be needed once the roofer verifies the damage onsite. It can also miss items. That's why the estimate isn't a final construction document. It's a claim valuation.

Practical rule: Compare scope before you compare totals. A lower price is fine if the roofing system, accessories, and workmanship standards still match what the home needs.

What to compare before you worry

Before you treat the gap as good news or bad news, compare these points line by line:

| Item to review | Insurance estimate | Contractor bid |

|---|---|---|

| Shingle area | Look for total measured area and waste | Confirm the measured repair area matches |

| Accessories | Check ridge cap, flashing, starter, underlayment | Make sure these aren't omitted |

| Labor setup | Often generalized | Should reflect actual access and complexity |

| Code items | May be limited or missing | Should note required ventilation or related work |

| Payment basis | ACV or RCV matters | Bid should be actual contract price |

If you're not sure whether the claim scope is complete, a documented roof evaluation helps. A detailed roof inspection report for insurance gives you something concrete to compare against the adjuster's worksheet.

A lower contractor bid isn't automatically a red flag. It becomes a problem only when the contractor gets there by stripping out needed components, using thinner scope, or planning to solve surprises later with change orders.

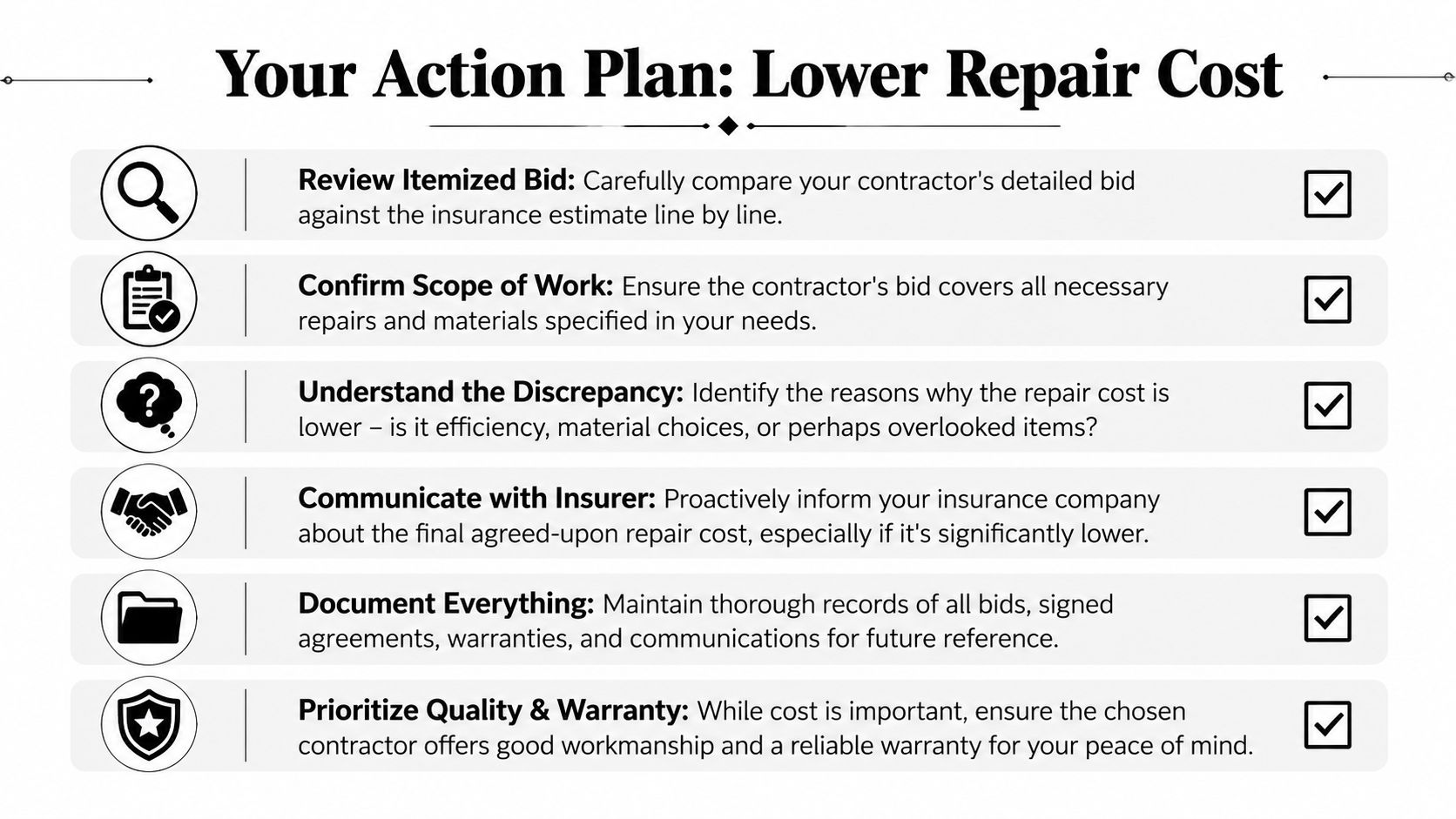

Your Action Plan When the Repair Cost is Lower

When the final repair price comes in below the insurance number, don't rush to spend the difference. Handle it like a claim manager would. Review the scope, protect your recoverable funds, and decide whether part of that money should improve the roof rather than just close the file.

Start with the paperwork

A structured approach works best. Key steps include getting itemized bids, checking for hidden damage that appears in 20 to 30% of initial inspections, and considering upgrades such as Class 4 impact-resistant shingles, which can improve hail resistance by 40 to 60%, according to this homeowner guide on repair cost versus insurance estimate.

Use this sequence:

Match the contractor bid to the adjuster scope.

Ask for an itemized proposal. Don't accept a one-line price if you're using insurance proceeds. You want materials, tear-off, flashing work, ventilation, cleanup, and warranty terms spelled out.Look for legitimate reasons the price is lower. Sometimes a roofer can repair efficiently because the damage is isolated, access is straightforward, or the insurer priced for broader replacement language than the roof needs.

Confirm what is not included.

Exclusions matter. Window trim, interior leak repairs, gutter guards, and decking replacement can sit outside the main roofing number. If those aren't included, the “savings” may not be real.

If the bid is lower because the contractor is more efficient, that can help you. If it's lower because critical components disappeared from the scope, it can hurt you later.

Decide how to use the difference wisely

If the work can be completed properly for less, homeowners often ask whether they can keep the remaining funds. In many situations, the answer is yes, subject to your policy terms, your mortgage company's requirements if applicable, and whether depreciation is still being held back.

Good uses for the difference include:

- Stronger materials: Upgrade to impact-resistant shingles if the roof and policy make that practical.

- Ventilation corrections: Improve intake and exhaust balance if the existing roof was under-vented.

- Related protection items: Replace aging flashing, pipe boots, or other small components that affect roof life.

- Reserve for claim closeout: Keep documentation and funds available until the carrier fully closes the file.

If your carrier pushes back unfairly, especially when there's confusion about payment rights or claim handling, it helps to understand broader legal options for denied insurance benefits. Most homeowners won't need that route, but knowing it exists changes how you approach a difficult claim conversation.

Keep a simple claim file

Organize one folder, paper or digital, with:

- The adjuster estimate: Every page, including summary and line items.

- Your roofing contract: Signed scope, price, and warranty details.

- Photos: Before, during, and after the repair.

- Invoices and proof of completion: These often control release of held-back funds.

- Email trail: Save insurer communications and supplement requests.

What doesn't work is casual recordkeeping. Homeowners lose money when they assume the insurer will ask for whatever it needs. Often, it won't. You have to submit the right documentation at the right time.

Handling Insurance Checks, Deductibles, and Depreciation

Many homeowners get stuck here because the first insurance check looks too low. That usually happens when the policy pays Actual Cash Value first, subtracts your deductible, and holds back depreciation until the work is complete.

Why the first check often feels too small

The insurer's first payment is often not the full claim value. It may represent the depreciated amount, less your deductible. That can make a claim feel underpaid even when the file is still open.

A simple example helps. Say the insurer values the roof loss higher than the first check suggests. The first payment may reflect ACV only. If your policy includes recoverable depreciation, the remaining funds aren't released until the carrier receives the final invoice or certificate of completion.

Many claims stall at that point. About 35% of homeowners forfeit their full depreciation recovery because they don't submit the final invoice or certificate of completion within the insurer's deadline, often 12 months, according to SK Roofing's explanation of insurance estimate disputes and depreciation recovery.

Submit completion paperwork as soon as the job is done. Waiting is one of the easiest ways to lose money you were otherwise entitled to collect.

How recoverable depreciation actually works

Treat recoverable depreciation as money with conditions attached. It's part of the settlement only after you prove the work was completed and the cost was incurred.

That means you should:

- Verify your policy type: ACV-only and RCV claims do not pay the same way.

- Know your deadline: Carriers often require final documentation within the claim window.

- Send final documents promptly: Invoice, certificate of completion, and photos are the usual package.

- Track deductible handling: Your deductible is still your responsibility and doesn't disappear because the repair price changed.

If you want a clearer view of the payment sequence, this overview of the roof insurance claim process helps homeowners understand what to expect from first inspection through final release of funds.

How to File a Supplement for a More Accurate Estimate

A homeowner approves a roof repair based on the carrier's first estimate, then the crew starts tear-off and finds bad decking at the eaves, missing flashing details, or ventilation work the adjuster did not include. That is a supplement situation.

A supplement is a request to correct the claim scope or pricing so the estimate matches the work the roof requires. It protects the homeowner from making up the difference for items that belong in the claim.

When a supplement makes sense

Some lower contractor bids are accurate. Others are lower only because the contractor is pricing the visible work while the insurer's estimate also has gaps, or because the insurer used pricing that does not reflect the local market. Labor is a common example. If Xactimate is set below what qualified crews are charging in Western Pennsylvania, the numbers on paper can look fine until the job is scheduled and real supplier and labor costs have to be covered.

Hidden conditions are another common trigger. We see supplements filed for decking replacement, step and counterflashing issues, multiple roof layers, starter and ridge omissions, and code-related ventilation corrections that become clear only after a closer inspection or tear-off.

That is normal roofing work, not claim inflation.

What strong supplement documentation looks like

A good supplement package is specific and easy for the adjuster to review. It should show the exact condition, the location, and the repair item needed to fix it properly.

Include:

- Annotated photos: Show the issue clearly and label the affected component.

- Line-item revisions: Match the carrier's estimate format so the adjuster can compare old scope to new scope quickly.

- Code references when required: If local code affects ventilation, flashing, ice protection, or other components, include the supporting language.

- Field notes from inspection or tear-off: Short, direct notes often explain hidden damage better than a generic summary.

- Material or labor support when pricing is off: Supplier quotes, crew rates, or similar local documentation can help justify the revision.

The goal is to make the supplement read like a construction record. Adjusters respond better to that than to broad complaints that the estimate is “too low.”

Homeowners can see the same documentation principles in other types of property claims. This guide on handling insurance after Phoenix home fires is useful because organized photos, clear timelines, and itemized scope changes matter in any insurance loss.

It also helps to choose a contractor who knows how to document real roof conditions, explain trade-offs before the job starts, and submit claim support in a format carriers recognize. If you are comparing companies, this guide on how to choose a roofing contractor for insurance-related repairs will help you ask better questions before you sign anything.

Penn Ohio Roofing & Siding Group handles this part of the process by tying field findings to the estimate line items, so the repair plan, claim paperwork, and final roof system stay aligned.

Partnering with Penn Ohio Roofing for a Successful Repair

A claim goes smoother when the contractor understands more than shingles. The work has to satisfy the roof system, the insurer's documentation requirements, and the local code environment at the same time.

What a qualified contractor should help you do

A useful roofing partner should help you compare estimate scope to real job scope, identify omissions before the contract is signed, and produce the paperwork needed to close out depreciation. That includes itemized proposals, completion documents, photos, and notes that make sense to a claims department.

The contractor should also be able to explain trade-offs plainly. For example, if a lower repair price leaves room for better underlayment, upgraded shingles, or ventilation improvements, that decision should be discussed before the work starts, not after materials arrive.

Tax questions are another area where homeowners need clarity. Keeping an insurance surplus is typically not taxable because it's reimbursement for a covered loss, but poor records can create problems if repair costs are also claimed as a casualty loss. That's why it makes sense to talk with a tax advisor, as noted in this discussion of roof repair surpluses and tax treatment.

If you're comparing contractors, use practical standards. Look at licensing, insurance, claim documentation habits, warranty clarity, and whether the company can explain your estimate without vague answers. This guide on how to choose a roofing contractor is a good place to start.

Frequently Asked Questions About Insurance Surpluses

Can I keep the difference if my roof repair cost less than insurance estimate

Often, yes. It depends on your policy, whether depreciation is still being withheld, and whether your mortgage company has a say in disbursing funds. The safer approach is to complete the work properly, keep records, and confirm the final claim handling in writing.

Can I use the extra money for something other than the roof

In many cases, homeowners can use remaining funds as they choose after the covered repair is completed and policy conditions are satisfied. The better question is whether that's the smartest use. Upgrades tied to roof durability usually deliver more value than unrelated spending.

What if the insurer asks for money back

Review your policy and payment paperwork. Some claims require proof of completed work before all funds are considered fully earned. If the carrier requests repayment, ask for the policy basis and claim calculation in writing before responding.

What if the lower bid missed something important

That's when you pause the job and review scope. A low number only helps if it still covers the full repair correctly. If the estimate is missing needed items, a supplement may be the right move.

If you're sorting through a claim and want clear answers before signing anything, Penn Ohio Roofing & Siding Group can help you review the scope, understand the payment process, and make a repair decision that protects your home for the long run.