You heard the storm. Then you heard the harder sound. A branch hit the roof, shingles snapped loose, or water started showing up where it never should. Now you're staring at the ceiling, your phone, and your policy, trying to figure out whether insurance will help or leave you holding the bill.

That's where most homeowners in Pennsylvania get stuck. Not because roof repair insurance coverage is impossible to understand, but because the answer isn't “yes” or “no.” It depends on the cause, the age of the roof, the policy language, the deductible, the documentation, and how well the damage is presented to the insurer. In places like Sharon, Pittsburgh, and Erie, where wind, hail, snow, and falling limbs all show up in real life, that nuance matters.

If you need a practical answer, here it is. Start with the cause of the damage. Then check how your policy values the roof. Then document everything before anyone disturbs the evidence. That order matters.

Table of Contents

- Your Guide Through the Storm

- What Your Homeowners Insurance Actually Covers

- Decoding Your Policy Deductibles Limits and Value

- Your Step-by-Step Roof Claim Workflow

- Why You Need a Professional Roofer on Your Side

- Handling Common Claim Denials or Lowball Offers

- Protecting Your Home in Hermitage Pittsburgh and Beyond

Your Guide Through the Storm

A lot of claims start the same way. A homeowner walks outside after a rough night, sees shingles in the yard, notices a limb hanging over the gutter, and wonders whether this is a simple repair or an insurance fight. The stress gets worse when water starts moving inside the house, because every hour feels expensive.

That stress is justified. Roof claims have become a much bigger issue for insurers and homeowners. The National Insurance Crime Bureau reported that convective storms caused about $60 billion in damage in 2023, double the previous year, and noted a major increase in hail-related claims at large insurers in its roof claims and storm-loss report. When losses rise like that, carriers respond by tightening terms and scrutinizing claims more aggressively.

That doesn't mean you should panic. It means you should be organized.

Practical rule: The homeowner who documents early, reads the valuation language, and gets a detailed roofing assessment usually stands in a much stronger position than the homeowner who just waits for the adjuster to decide everything.

In Pennsylvania, that matters even more because roof problems don't all look the same. A house in Erie may deal with snow load and ice issues. A home near Pittsburgh may take wind damage from a fast-moving storm. In Sharon, Hermitage, and nearby communities, tree strikes and shingle blow-offs are common enough that homeowners need to know what counts as a covered event and what insurers will call maintenance.

If you treat this like a paperwork problem only, you'll miss the roofing side. If you treat it like a roofing problem only, you'll miss the insurance side. You need both.

What Your Homeowners Insurance Actually Covers

The biggest mistake homeowners make is starting with the repair. Insurance starts with the cause of loss.

The rule adjusters start with

Most homeowners policies cover roof damage when a covered peril causes sudden, accidental damage. Consumer guidance from Policygenius explains that covered causes generally include events like wind, hail, fire, or a fallen tree, while poor maintenance and normal aging usually aren't covered. It also notes that roofs older than 20 years may receive reduced coverage, often based on depreciated value instead of full replacement cost, as explained in Policygenius's roof damage coverage guide.

That one rule answers most roof claim questions.

A windstorm tears shingles off a roof. That usually points toward coverage. A branch punches through the decking. That usually points toward coverage. A slow leak that's been staining the attic for months because flashing failed and nobody fixed it. That often points toward denial.

If you want a plain-English explanation focused on leak situations, ISU Insurance Services' guide to roof leaks is worth reading because leaks confuse people more than almost any other claim type.

If the damage happened all at once, you may have a claim. If it happened slowly over time, expect pushback.

Roof damage coverage at a glance

| Cause of Damage | Typically Covered? | Reason |

|---|---|---|

| Wind lifting or tearing shingles | Usually yes | Sudden damage tied to a covered weather event |

| Hail impact | Usually yes | Hail is commonly treated as a covered peril |

| Fire damage | Usually yes | Fire is a standard covered peril in many policies |

| Falling tree branch | Usually yes | The damage comes from a distinct accidental event |

| Old shingles reaching end of life | Usually no | Aging and wear are maintenance issues |

| Ongoing leak from neglected flashing | Usually no | Progressive deterioration is commonly excluded |

| Pest-related damage | Usually no | Policies commonly exclude this type of loss |

| Flood-related roof damage | Usually no under standard homeowners coverage | Flood is typically excluded from standard policies |

| Earthquake-related roof damage | Usually no under standard homeowners coverage | Earthquake is typically excluded from standard policies |

A smart homeowner asks three questions before filing:

- What happened first: Identify the actual event. Storm, hail, tree strike, fire, or something gradual.

- What can I prove: If you can't connect the damage to a specific event, the claim gets weaker fast.

- How old is the roof: Older roofs face more scrutiny, and that changes the payout even when the event is covered.

If you answer those, you'll have a much better sense of whether your roof repair insurance coverage issue is a legitimate claim or a maintenance bill.

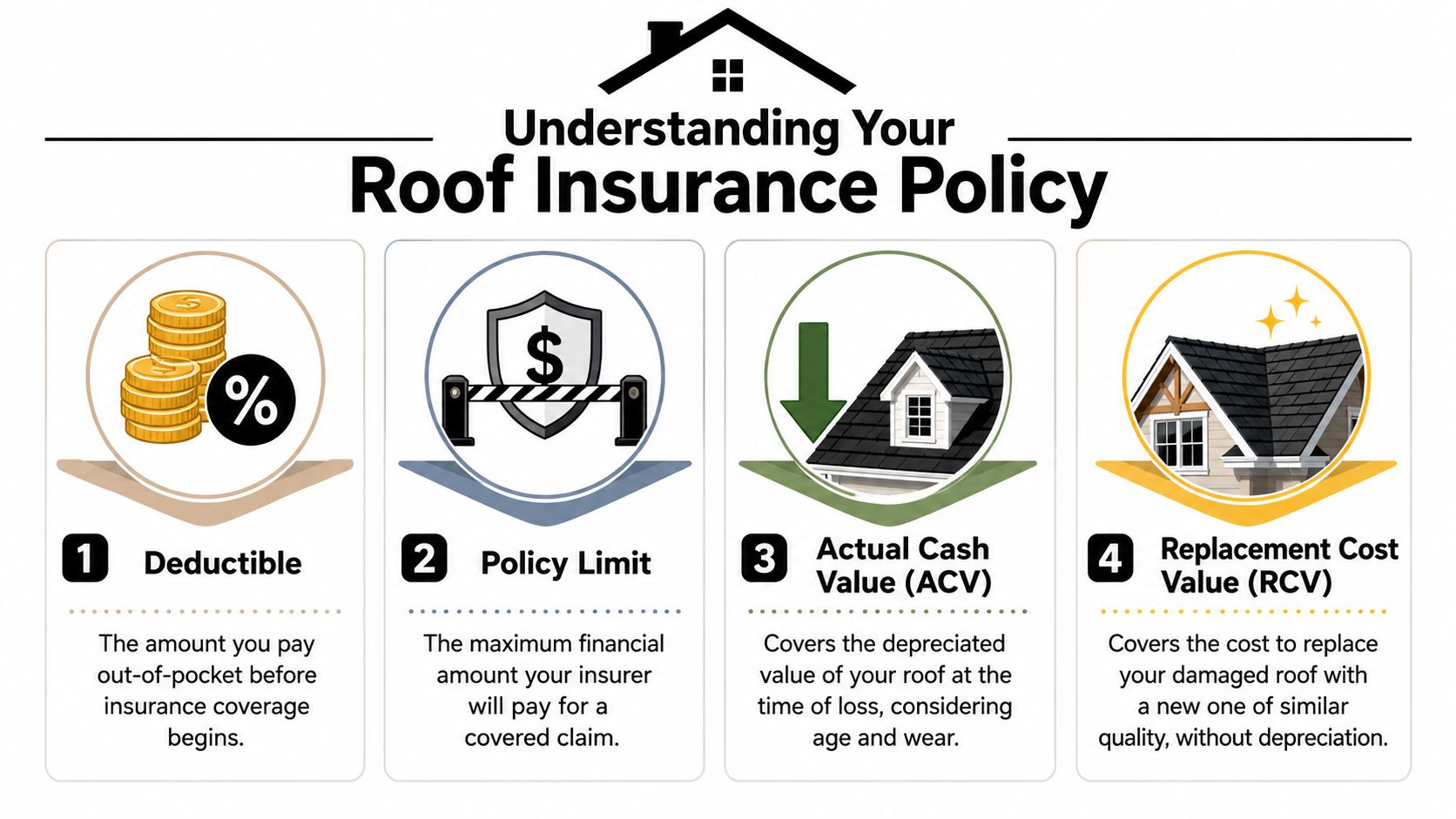

Decoding Your Policy Deductibles Limits and Value

A covered claim still doesn't guarantee a full check. The final number comes down to how your policy values the roof and what you must pay first.

The three numbers that control your payout

Start with the deductible. That's your out-of-pocket share before coverage applies. If the damage is minor and the repair total sits close to the deductible, filing may not make sense.

Then look at the policy limit. The roof usually falls under dwelling coverage, but payment still stays within policy limits and exclusions. If the repair scope grows because decking, underlayment, or interior water damage is involved, limits matter.

Then comes the valuation method. Homeowners often get blindsided.

If you want a contractor-focused explanation of what insurers look for in damage valuation, a formal roof inspection report for insurance claims can help you understand what should be documented before the adjuster finalizes the scope.

Why ACV hurts older roofs

Many carriers don't value an older roof the same way they value a newer one. Guidance summarized by Texcoro notes that many policies shift older roofs from replacement cost value (RCV) to actual cash value (ACV), which subtracts depreciation and can sharply reduce what the insurer pays, as outlined in Texcoro's explanation of ACV vs. RCV for roof claims.

When a car that has been on the road for years is totaled, the insurer doesn't usually pay what a brand-new version costs. ACV works the same way on a roof. The roof may need a full new replacement, but the policy may only pay for the roof's depreciated value at the time of loss.

That's why homeowners with older homes in Western Pennsylvania need to stop asking only, “Is storm damage covered?” The harder question is, “How will my insurer value this roof?”

A few practical checks:

- Read the settlement language: Look for ACV, RCV, recoverable depreciation, and roof-age endorsements.

- Check for separate wind or hail terms: Some policies treat storm losses differently than other covered events.

- Confirm roof age documentation: If the insurer has the wrong installation date, your payout can suffer.

- Compare estimates carefully: If the insurer's scope is light, the valuation problem gets worse.

For a broader homeowner view of how hail damage can affect repair decisions and cost expectations, Cover Club's hail damage insights can be a helpful secondary reference.

Your Step-by-Step Roof Claim Workflow

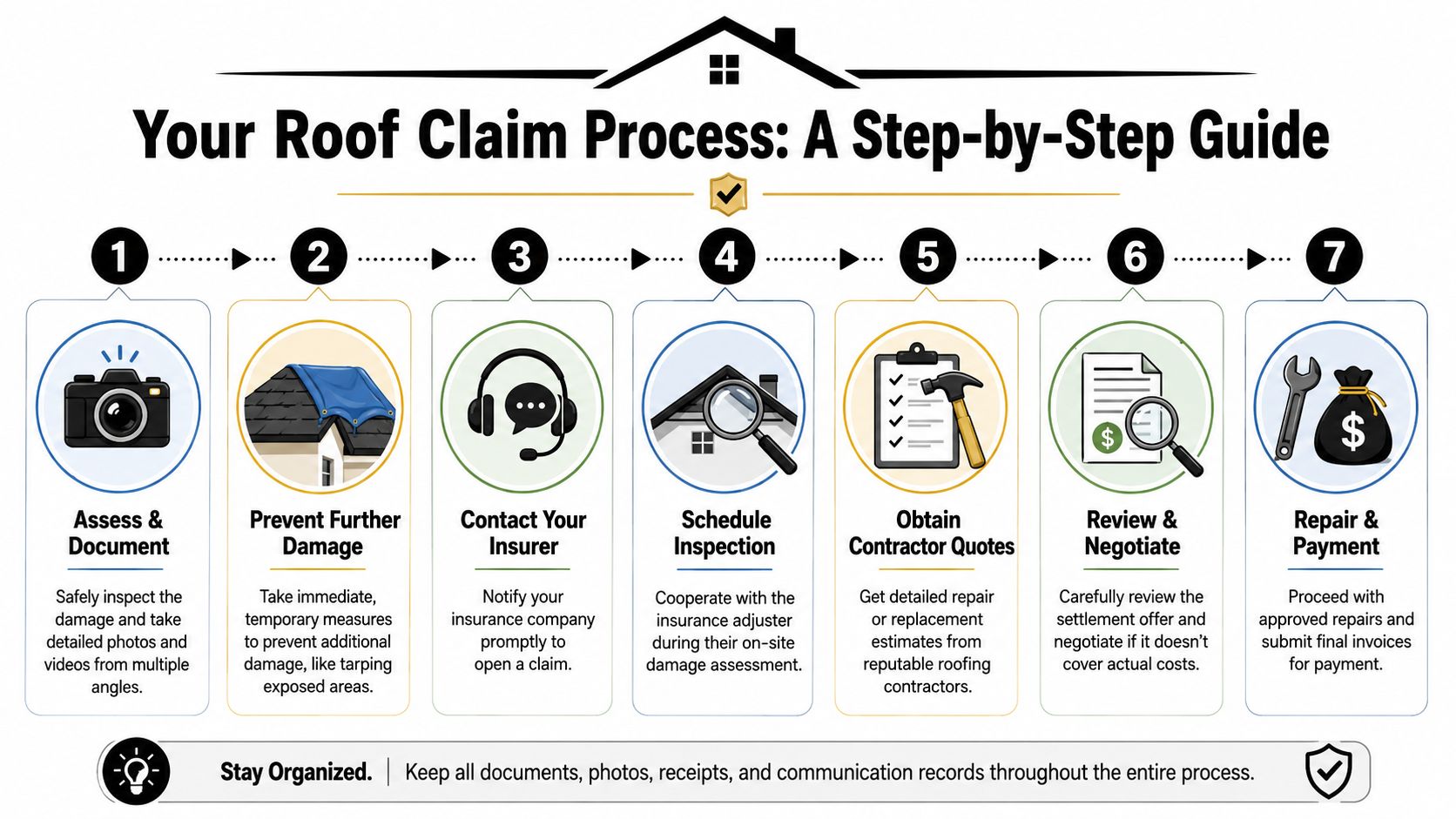

When damage happens, speed matters. Sloppy speed causes mistakes. Organized speed wins claims.

What to do before you call

Kin's consumer guidance is clear on this point. Strong roof claims usually start with immediate photos and videos, temporary steps to prevent more damage, and saved receipts for anything spent to protect the property, as explained in Kin's roof repair insurance advice.

Do these first:

- Make sure the area is safe. Don't climb a damaged roof after a storm. Use binoculars from the ground, take yard-level photos, and check ceilings and attic spaces inside.

- Photograph everything before cleanup. Get wide shots of the house, close-ups of missing shingles, dented metal, fallen limbs, exposed underlayment, and interior staining.

- Shoot video too. Video gives context. Walk the perimeter, narrate what you see, and capture dates if possible.

- Stop further damage. Tarp exposed areas if it can be done safely. Preventing water intrusion is part of your responsibility.

- Save every receipt. Tarping, emergency service, cleanup materials, temporary sealing, and contractor emergency invoices all matter.

Use a folder on your phone and email backups to yourself. Don't rely on one device.

Don't wait for the adjuster to tell you what existed. Build the record yourself on day one.

If you want a localized overview of the full process homeowners follow after storm loss, this roof insurance claim process guide lays it out in a way that matches how claims usually unfold in the field.

What happens after the claim opens

Once you report the loss, stay disciplined. Don't ramble. Give the date of loss, the event you believe caused it, and the visible damage you observed.

Then prepare for inspection.

- Have your evidence ready: Photos, videos, receipts, and a written timeline.

- Request the adjuster's scope in writing: You need to compare their findings to the roofer's findings.

- Get a detailed contractor estimate: A vague one-page quote won't help if there's a dispute.

- Review the settlement carefully: Check line items, materials, disposal, flashing, underlayment, and code-related items if applicable.

- Ask questions immediately: If something obvious is missing, challenge it before repairs move too far.

The homeowners who struggle most are usually the ones who moved too quickly, threw away damaged materials, failed to document temporary repairs, or accepted a scope they didn't understand.

Why You Need a Professional Roofer on Your Side

A roof claim is not just an insurance file. It's a building-performance issue with insurance consequences. That's why bringing in a qualified roofer early is one of the smartest moves you can make.

A roofer does more than repair shingles

An adjuster evaluates coverage. A roofer evaluates the roof.

Those are not the same job.

A professional roofer can identify brittle shingles, lifted seal strips, flashing displacement, soft decking, ridge damage, underlayment exposure, and collateral issues the homeowner may never notice from the yard. That matters because many claim disputes start with incomplete damage identification, not just policy language.

In practical terms, the roofer becomes your fact witness on the condition of the roof. They can document storm-created openings, distinguish fresh impact from old deterioration, and explain why a “simple repair” may not restore the roof system.

What a good roofing report should include

Don't settle for a handshake opinion. Ask for a report with substance.

A useful insurance-facing roofing assessment should include:

- Cause-based observations: What points toward wind, hail, falling debris, or another event

- Photo documentation: Clear images tied to roof slopes, elevations, and components

- Repairability analysis: Whether the damaged section can be repaired without creating a mismatch or performance problem

- Material identification: Shingle or roofing type, visible age condition, and availability concerns

- Written scope of work: Specific items, not vague “repair roof” language

One local option that may be useful is Penn Ohio Roofing & Siding Group, which states that it works with insurance companies, provides claim-related guidance, and helps compare a roofer's scope with the adjuster's findings. That kind of documentation support is especially useful for homeowners in Mercer, Beaver, and Lawrence County who need field evidence, not just opinions.

A strong roofer doesn't argue emotionally with the insurer. They document the roof so the insurer has a harder time ignoring the facts.

If your claim involves visible damage plus uncertainty about what lies beneath, professional documentation isn't optional. It strengthens your claim.

Handling Common Claim Denials or Lowball Offers

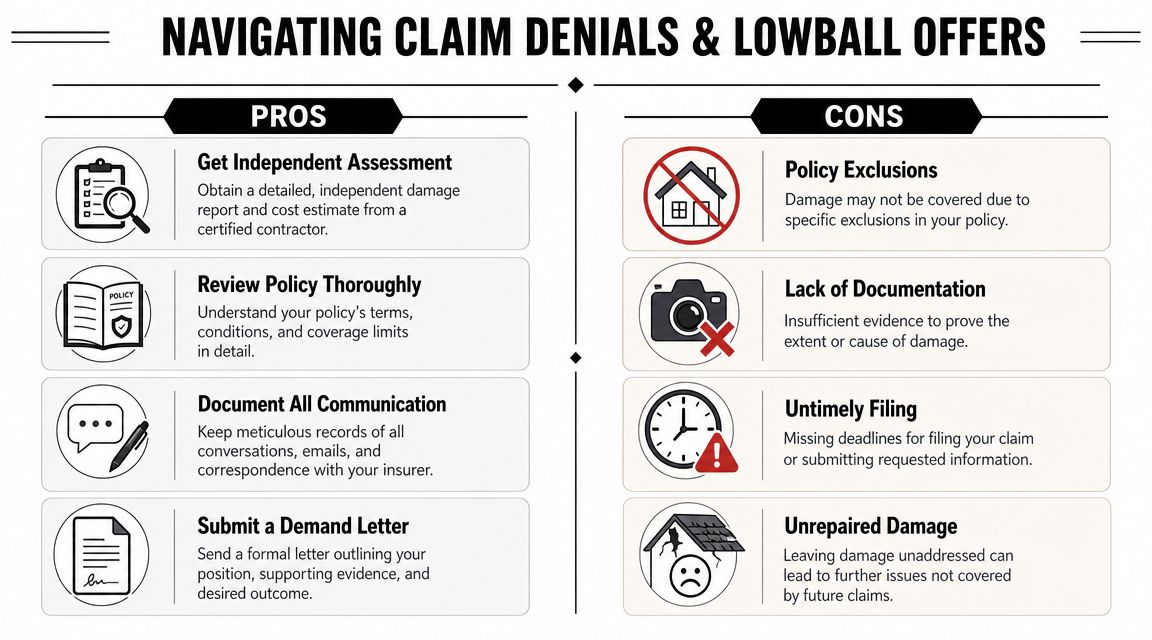

Insurers deny claims for reasons. Some are valid. Some are weak. Your job is to know the difference.

When the insurer says repair only

One of the toughest Pennsylvania disputes involves matching. The insurer agrees some damage exists but only wants to pay for a repair on one slope or one section. That sounds fine until the replacement shingles don't match the existing roof in color, profile, texture, or even performance.

Property Insurance Coverage Law summarizes a Pennsylvania appellate discussion showing that when a homeowner can prove a “reasonably matching” shingle isn't available, the repair-versus-replacement question can become a real factual dispute, as discussed in its analysis of repair versus replacement in Pennsylvania roof claims.

That matters a lot for older homes. If the material is discontinued or the weathered roof can't be matched in any reasonable way, a partial patch may leave the house with a visibly inconsistent roof. In some cases, that pushes the argument toward full replacement.

Other common denial themes include:

- Wear and tear: The insurer says the roof failed from age, not the storm

- Pre-existing damage: They argue the condition existed before the reported event

- Insufficient proof: The file lacks enough photos, timeline evidence, or contractor detail

- Damage below deductible: Covered damage exists, but payment doesn't exceed the deductible

How to push back the right way

Don't answer a weak decision with anger. Answer it with paper.

Start here:

- Request the denial or low offer in writing. You need the exact policy basis, not a vague phone explanation.

- Compare scopes line by line. Missing accessories, flashing, starter, ridge components, or tear-off details often explain low offers.

- Get an independent roofing report. If the issue is causation or repairability, expert documentation changes the conversation.

- Document communication. Keep emails, call logs, names, dates, and follow-up summaries.

- Submit a focused rebuttal. Attach photos, contractor findings, material availability evidence, and the policy language you believe supports payment.

If the dispute escalates beyond ordinary back-and-forth, homeowners sometimes need to understand broader legal options for denied claims so they know what formal next steps may exist.

A low offer isn't automatically bad faith. But it also isn't automatically correct. If the insurer's scope doesn't restore the roof properly, challenge it before work starts and before the record hardens against you.

Protecting Your Home in Hermitage Pittsburgh and Beyond

Roof repair insurance coverage gets easier when you strip away the noise. Ask what caused the damage. Check how the policy values the roof. Document everything immediately. Bring in a roofer who can prove what happened and what proper repair requires.

That advice isn't theoretical in this region. Homes around Erie face lake-effect snow and freeze-thaw stress. Properties near Pittsburgh see hard wind events and storm-driven debris. In Hermitage and Sharon, older housing stock and mature trees create a mix of impact damage, shingle loss, and difficult matching issues after partial repairs.

Your next move should be simple:

- If the damage is active, protect the home first

- If the cause looks storm-related, open the claim promptly

- If the roof is older, verify whether ACV or RCV applies

- If the insurer's scope feels light, get a second set of eyes

For homeowners who need local repair help after a covered event or a denied claim dispute, reviewing a nearby roof repair service in Hermitage, PA can help you move from uncertainty to an actual inspection and written scope.

A roof claim is stressful, but it's manageable when you treat it like a documentation job from the first hour and a roofing job from the first inspection.

If your roof was damaged by wind, hail, a fallen tree, or another sudden event, talk to Penn Ohio Roofing & Siding Group for an inspection, claim documentation support, and a clear plan for repair or replacement.